Palantir is one of those stocks where the debate never really goes quiet.

Bulls see one of the clearest software winners in the AI cycle. Bears see a great company with a stock price that already assumes a lot has to go right. Both sides have a point.

What makes PLTR interesting in 2026 is that the company is no longer selling investors only a story. The growth is showing up. Government demand remains strong. U.S. commercial adoption is accelerating. AI is moving from presentation slides into real contracts and operating systems.

But the stock market is not paying Palantir like an undiscovered opportunity. It is paying for speed, execution, and a very long runway. That makes PLTR one of the more important AI stocks to watch — and one of the harder ones to trade casually.

Palantir Is Not Just Another AI Stock

A lot of public companies have tried to attach themselves to the AI trade. Palantir is different because AI is already close to the center of what it sells.

The company’s pitch is not just “use AI to work faster.” It is more specific: help governments, defense agencies, and large companies turn messy data into decisions. That can mean logistics, intelligence, planning, fraud detection, supply chains, battlefield systems, or enterprise workflows.

That is why investors treat PLTR differently from many software names. Palantir is not simply selling dashboards. It is trying to become part of how large organizations operate.

That is a powerful position to have if operational AI becomes a long-term spending cycle rather than a short burst of hype.

The Business Is Delivering

The strongest argument for PLTR is simple: the numbers have been strong.

Recent results showed fast revenue growth, especially in the U.S. business. Government demand remains a major support, while commercial growth has become harder to ignore. That matters because one of the old criticisms of Palantir was that it depended too much on government contracts.

That argument is getting weaker.

If more private-sector customers keep moving from AI experiments into larger Palantir deployments, the market will have a stronger reason to view PLTR as a broad enterprise AI platform, not just a government analytics company.

That is the bullish case in plain English. Palantir is proving that AI can become revenue.

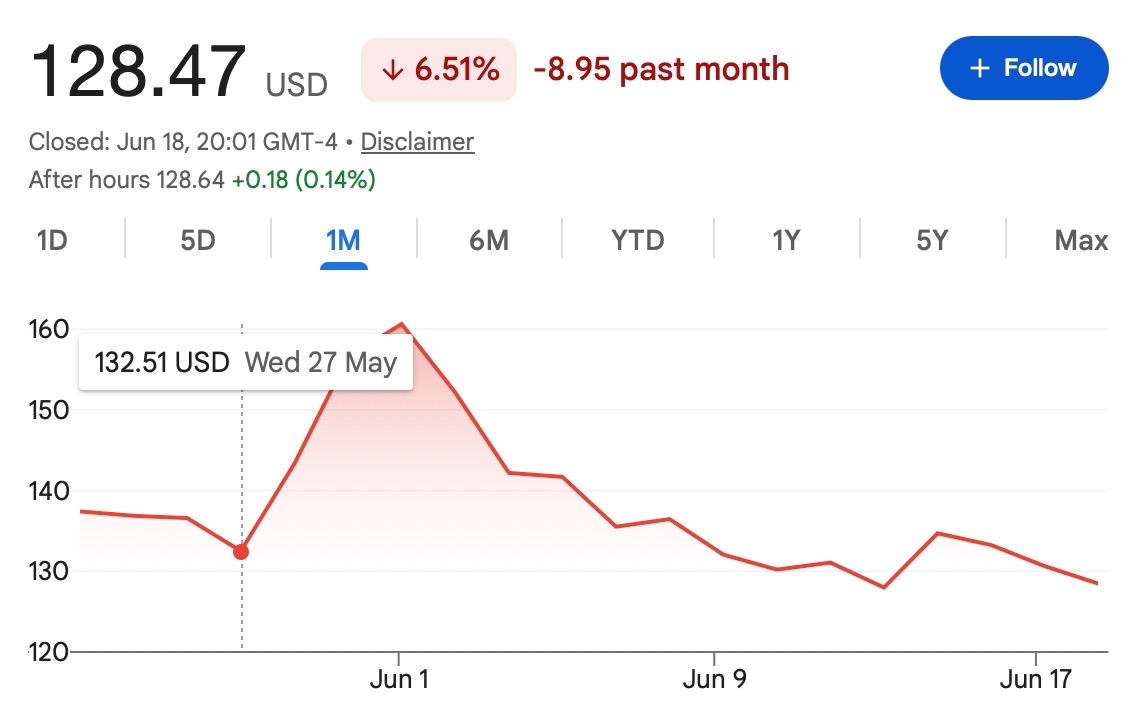

The Valuation Is the Problem

The problem is not that Palantir lacks a story. The problem is that the market already believes the story.

PLTR still trades like a premium AI growth stock. That means good results may not always be enough. Investors may want faster growth, better margins, bigger customer wins, stronger guidance, and continued proof that AI demand is durable.

That is a tough bar.

This is why PLTR can fall even after decent news. When expectations are high, the stock is not judged only by whether the company is improving. It is judged by whether the company is improving faster than the market already expected.

That is the part newer traders often miss. A strong company can still be a risky trade if the valuation leaves little room for disappointment.

Government Demand Is Still a Major Advantage

Palantir’s government business remains one of its biggest strengths.

Defense, intelligence, national security, and public-sector data systems are not easy markets to enter. Once software becomes deeply embedded in mission-critical workflows, it can be difficult to replace.

That gives Palantir a real advantage. Large government contracts also help support the idea that Palantir is not selling optional software. In many cases, its tools are connected to serious operational needs.

But this side of the business also comes with baggage. Government procurement can be political. Data systems can be controversial. Public-sector contracts can face scrutiny around privacy, surveillance, transparency, and national dependence on U.S. technology vendors.

For Palantir, the same government exposure that creates trust with investors can also create headline risk.

Commercial Growth Is the Key Test

The next chapter for PLTR probably depends on commercial adoption. Government contracts can support the base. Commercial growth is what can expand the ceiling.

Investors want to know whether Palantir can become a normal part of enterprise AI spending across industries. Not just pilots. Not just small tests. Real deployments. Bigger contract values. More repeat usage. More customers using Palantir as part of daily operations.

That is where the stock’s upside case becomes more convincing.

If commercial growth keeps accelerating, PLTR can continue to trade like one of the few software companies actually monetizing AI at scale.

If that growth slows, the valuation conversation will come back quickly.

Why PLTR Can Stay Volatile

PLTR is not the kind of stock that moves only on company news.

It also reacts to the broader AI trade, Nasdaq sentiment, software valuations, interest-rate expectations, government spending headlines, and analyst commentary.

That makes the stock sensitive from several directions at once.

If investors are willing to pay up for AI software, PLTR can catch a strong bid. If the market starts questioning growth multiples, PLTR can get hit even if the company itself is still performing well.

This is why traders need to separate the company from the stock.

Palantir may remain one of the strongest AI software companies in the market. That does not mean every entry price is attractive, and it does not mean the stock cannot drop sharply during valuation resets.

Bottom Line

Palantir is still one of the most important AI software names in the market.

The company is growing. The government business remains strong. Commercial adoption is improving. The AI story is more real here than it is for many companies trying to ride the same theme.

But PLTR is not priced for average execution. It is priced for a company that has to keep winning.

That is why the stock remains both exciting and dangerous. The upside case is clear if AI demand keeps turning into revenue and commercial customers continue to scale. The downside risk is also clear if valuation pressure returns or growth fails to exceed expectations.

Explore the latest markets on Tapbit, log in to trade, or create an account to get started.

Frequently Asked Questions (FAQ)

Is Palantir still a strong AI stock in 2026?

Yes, Palantir remains one of the most closely watched AI software stocks in the market. Its strength comes from government contracts, defense-related data systems, and growing commercial demand for operational AI. The bigger debate is not whether Palantir has an AI story, but whether PLTR can keep growing fast enough to support its valuation.

Why is PLTR so popular with investors?

PLTR is popular because it sits at the intersection of AI, data analytics, defense technology, government operations, and enterprise automation. Unlike some companies that only talk about AI, Palantir has already turned AI and data infrastructure into real contracts and revenue growth.

Is PLTR a cheap stock after its pullback?

Not necessarily. A lower price compared with previous highs does not automatically make PLTR cheap. The stock still trades with premium AI-growth expectations, which means investors are paying for strong future execution.