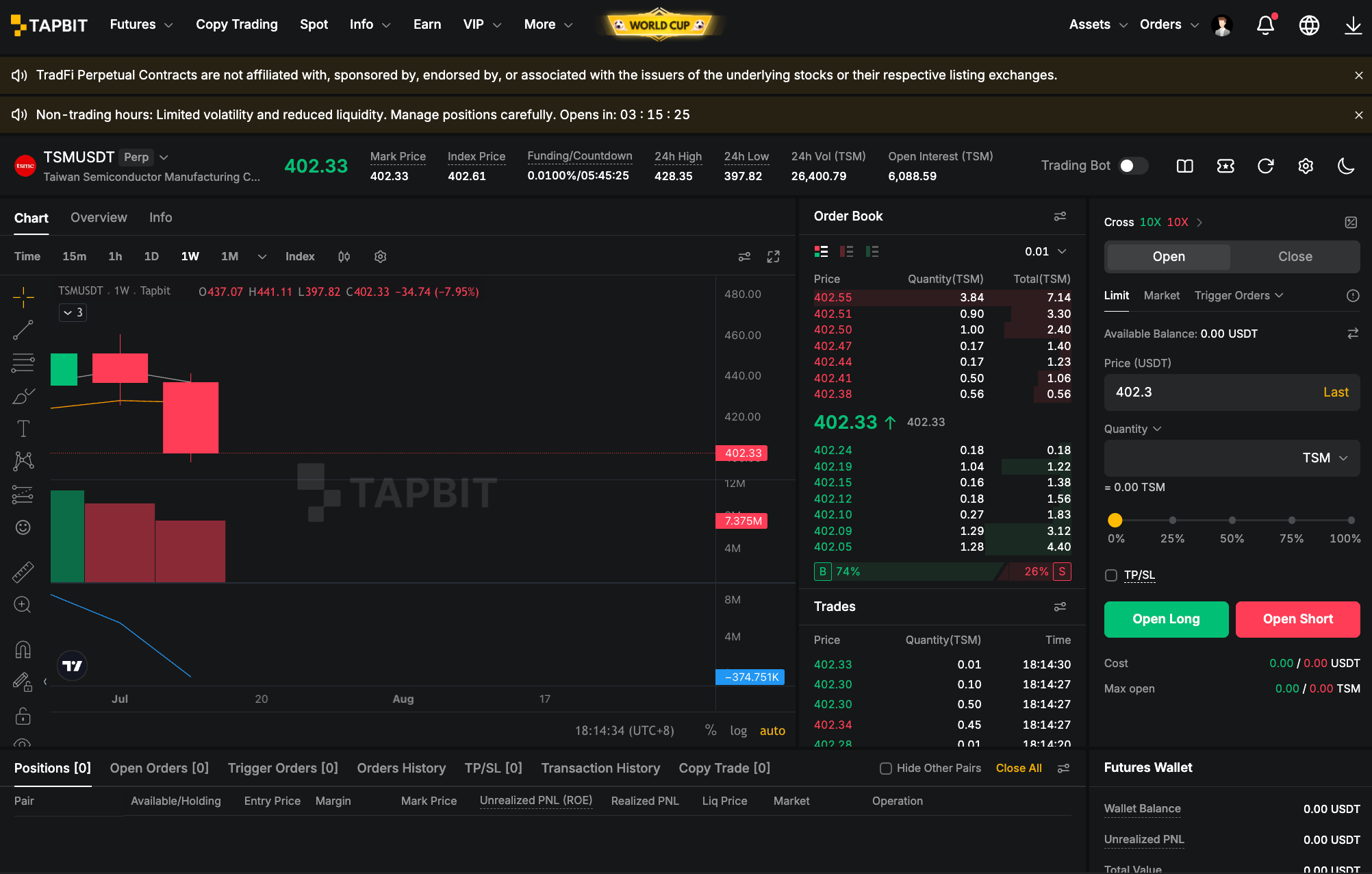

TSMC earnings delivered almost everything an AI-chip bull could ask for: record quarterly profit, faster revenue growth, stronger third-quarter guidance and another major expansion commitment. Yet the first market reaction was not a simple celebration. TSM's U.S.-listed shares traded near $419.48 and initially fell after the release, showing that the stock is now being judged against exceptionally high expectations rather than merely good results.

That tension is the real story. Taiwan Semiconductor Manufacturing Company earned NT$706.6 billion, roughly $22 billion, in the second quarter of 2026, up 77% from a year earlier. Revenue reached about $40.2 billion, up 36%, and earnings per ADR came in around $4.31, above the market consensus reported before the release. The company also guided third-quarter revenue to $44.6 billion-$45.8 billion, above the prevailing analyst estimate. These are not marginal beats; they show that AI infrastructure spending is still flowing into advanced manufacturing at scale.

TSMC Q2 2026 Earnings: The Numbers That Matter

The headline profit figure is important, but the revenue mix explains why the result matters to investors. According to TSMC's quarterly disclosures, advanced technologies accounted for 77% of wafer revenue. The 3nm node represented 30%, while the newly ramping 2nm node contributed 3%. That mix suggests customers are not merely ordering more chips; they are moving toward the most expensive and technically demanding manufacturing processes.

High-performance computing remained the central growth engine. Reuters reported that management expects full-year revenue growth of more than 40%, supported by demand from cloud providers and AI-chip customers. The next-quarter revenue midpoint of $45.2 billion implies another sequential increase of roughly 12% from Q2. Investors should therefore monitor whether revenue growth remains broad enough to absorb the cost of capacity expansion rather than focusing only on one quarter's profit beat.

Gross margin reached 67.7%, a record level, but guidance for Q3 moved to 65%-67%. That slight step-down helps explain the cautious stock reaction. It does not indicate weak demand; it indicates that overseas manufacturing, ramp costs and heavy capital investment may prevent every dollar of additional revenue from flowing directly to margin. TSMC raised its 2026 capital-spending range to $60 billion-$64 billion and announced another $100 billion of U.S. investment, bringing total U.S. commitments to about $265 billion.

Why TSM Fell Despite a 77% Profit Increase

A stock can fall after a strong report when the result confirms what investors already expected. TSMC entered earnings as the dominant manufacturer for Nvidia, Apple, AMD and other advanced-chip customers. The market already understood that AI demand was strong. The more difficult question was whether TSMC could beat rising expectations without creating new margin or capital-intensity concerns.

The initial decline therefore looked less like a rejection of the AI thesis and more like a repricing of the cost required to sustain it. A $60 billion-$64 billion capital budget and a $265 billion U.S. expansion commitment improve long-term capacity and geopolitical diversification, but fabs in Arizona may carry higher labor, construction and operating costs than comparable Taiwanese capacity. Investors now need evidence that overseas scale can improve without permanently diluting TSMC's margin advantage.

Expectations are also unusually elevated. MarketWatch cited a fund manager describing expectations as exceptionally high. When a stock is priced for continuous upside surprises, a record quarter can still produce profit-taking if guidance, gross margin or cash deployment does not exceed the most optimistic assumptions.

Three Signals to Watch After TSMC Earnings

1. Can TSM Hold the $410 Area and Reclaim Recent Highs?

TSM was trading near $419.48 after the report. The first practical reference is the $410 area, which sits close to the post-earnings support zone discussed by traders. Holding above it would suggest that the initial decline was profit-taking rather than the start of a larger earnings reset. A recovery through the recent $429 area would provide stronger confirmation that buyers are willing to pay for the upgraded growth outlook.

A sustained break below $410 would not invalidate TSMC's business strength, but it would warn that valuation and margin concerns are dominating near-term price action. Price confirmation matters because a strong company can remain a poor short-term entry when expectations are too crowded.

2. Does 2nm Ramp Without Damaging Margin?

Two-nanometer production contributed 3% of wafer revenue in the quarter, while 3nm contributed 30%. The next phase of the investment case depends on how quickly 2nm scales and whether customers accept premium pricing. Investors should track the node's revenue contribution, utilization and margin commentary over the next two quarters.

3. Can Advanced Packaging Keep Up With AI Demand?

AI accelerators need more than leading-edge wafers. They also rely on advanced packaging and high bandwidth memory to connect compute and memory efficiently. A shortage in CoWoS or HBM can limit complete-system shipments even when wafer demand is strong. Tapbit Learn's AI memory trade guide explains why this bottleneck links TSMC's outlook with Nvidia, SK Hynix and Micron.

TSM Bull, Base and Bear Scenarios

| Scenario | Evidence Required | What Would Weaken It |

|---|---|---|

| Bull | TSM reclaims roughly $429, Q3 revenue reaches the upper end of guidance, 2nm and CoWoS scale without a sharper margin decline. | Capex rises again while free-cash-flow conversion or gross margin disappoints. |

| Base | Shares consolidate around $410-$429 while earnings estimates rise gradually and investors absorb U.S. expansion costs. | A decisive break from the range with worsening estimate revisions. |

| Bear | TSM loses $410, Q3 margin falls below guidance or hyperscaler AI spending slows. | A rapid price recovery backed by stronger margins and customer demand. |

How to Trade TSM-USDT on Tapbit

Tapbit lists TSM-USDT stock-linked futures for traders seeking price exposure to TSM. It is a derivative contract, not direct ownership of TSMC shares, and it does not provide shareholder voting rights or dividends.

- Create an account and open the TSM-USDT futures market.

- Review the contract specification, index price, liquidity, funding and leverage before entering.

- Choose the order type and size the position around a defined support, confirmation and invalidation level.

- Confirm the order and manage the trade with a predefined stop and exit plan.

Final Assessment

TSMC's quarter confirms that AI demand is still producing extraordinary operating results. The company is not struggling to find demand; it is managing the cost and complexity of meeting it. That makes the stock decision more nuanced than simply buying a 77% profit increase. A stronger setup requires price confirmation, successful 2nm and packaging expansion, and evidence that record capital spending can preserve TSMC's margin advantage.

Frequently Asked Questions

What were TSMC's Q2 2026 earnings?

TSMC reported net profit of NT$706.6 billion, up 77% year over year, and revenue of about $40.2 billion, up 36%.

Why did TSM stock fall after strong earnings?

The market had already priced in powerful AI demand. Investors focused on slightly lower next-quarter margin guidance, very high expectations and the cost of TSMC's expanded U.S. investment program.

What is the most important TSM price level after earnings?

The $410 area is an initial support reference, while a sustained move above the recent $429 area would provide stronger recovery confirmation.

Does TSM-USDT give investors TSMC shares?

No. TSM-USDT is a stock-linked futures contract that provides derivative price exposure, not direct ownership, voting rights or dividends.