SK Hynix has become one of the clearest winners of the AI boom. That may sound strange at first. When people talk about AI stocks, they usually start with Nvidia, cloud companies, chip designers or data center operators. Memory used to be treated as a cyclical business — important, but often volatile and easy to overlook.

That has changed. The reason is high-bandwidth memory, better known as HBM. AI chips need huge amounts of fast memory to move data efficiently. Without advanced memory, even the most powerful accelerators cannot perform at full strength. As demand for AI servers has exploded, HBM has moved from a specialist semiconductor product into one of the most important bottlenecks in the AI supply chain.

SK Hynix was early to that opportunity. The company built a strong position in HBM and became a key supplier for Nvidia’s AI platforms. That has transformed how investors look at the stock.

The market no longer sees SK Hynix as just another memory maker. It sees the company as an AI infrastructure supplier. That explains the rally. It also explains why the stock is now more difficult to trade.

SK Hynix Is Riding the HBM Wave

The bull case for SK Hynix is simple: AI systems need more advanced memory, and SK Hynix is one of the companies best positioned to supply it.

HBM is not ordinary DRAM. It is more complex, harder to produce and more valuable to customers building advanced AI chips. That has given SK Hynix pricing power and helped push margins to levels that would have looked unusual in earlier memory cycles.

The company’s recent financial results showed how powerful this shift has become. Revenue and profit have surged, supported by HBM demand, high-capacity server DRAM and enterprise SSD sales. These are not just “good memory market” numbers. They reflect a market where AI infrastructure spending is changing the earnings profile of the business.

That is why investors have been willing to reprice the stock so aggressively. SK Hynix is no longer trading only on the old DRAM cycle. It is trading on the belief that AI memory demand could stay tight for longer than previous memory upcycles.

That belief may still be right. But after such a large move, the stock now needs continued proof.

Nvidia Is Still the Center of the Story

A big part of SK Hynix’s rise is connected to Nvidia. Nvidia’s AI platforms need advanced memory, and SK Hynix has been one of the most important HBM suppliers in that ecosystem. When Nvidia demand keeps rising, investors naturally look for companies that benefit from the same spending cycle.

SK Hynix has been one of them.

But this is where the story becomes more nuanced. Nvidia does not want to depend on one supplier forever. It has every reason to work with multiple memory partners, including Samsung and Micron. A broader supply base reduces risk, improves flexibility and helps Nvidia secure enough capacity for future AI platforms.

That does not mean SK Hynix loses its lead overnight. It does mean traders should stop thinking of the company as having a guaranteed monopoly on the AI memory trade. HBM4 qualification, next-generation platform timing, customer allocation and production yields will all matter more from here.

When a stock has already priced in leadership, simply being strong is not enough. It has to stay ahead.

The Stock Has Become a Crowded Trade

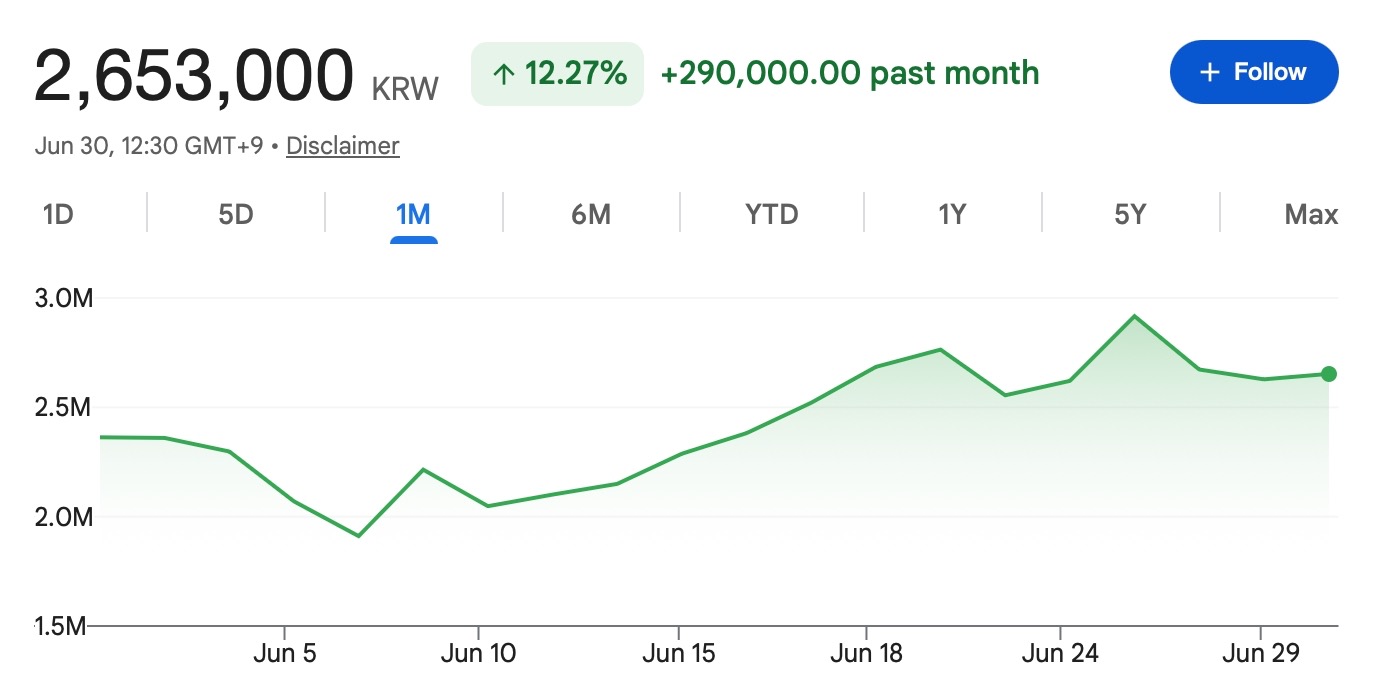

SK Hynix is no longer a quiet AI beneficiary. The stock has already rallied sharply this year, and recent price action shows how crowded the trade has become. Big daily moves in both directions suggest that investors are reacting quickly to every headline about Nvidia, HBM supply, Samsung, Micron or AI capex.

That is what happens when a stock becomes a market favorite.

The same story that attracts buyers can also make the stock fragile. If everyone is already positioned for strong HBM demand, then even a small doubt can trigger a large reaction. A report about slower capacity expansion, a rival gaining ground, or a change in Nvidia’s platform schedule can quickly move the stock.

This does not mean the AI memory story is over. It means the margin for error is smaller. A year ago, investors may have been discovering the HBM opportunity. Now, they are debating how much of that opportunity is already reflected in the share price.

That is a very different trade.

Memory Is Still a Cycle

The biggest mistake traders can make is assuming HBM has permanently ended memory cyclicality.

It has not.

HBM is a better business than commodity DRAM right now. Supply is tight, demand is strong and the product is tied to one of the biggest investment themes in the world. But memory has always been a capital-intensive industry. When margins are high, companies invest. When demand looks strong, capacity expands. When competitors see an opportunity, they chase it.

That cycle may take time to play out in HBM because qualification is difficult and customers need reliable suppliers. SK Hynix still has an advantage. But Samsung and Micron are not standing still. Both companies are investing aggressively in next-generation HBM, and Nvidia’s multi-supplier approach gives them a reason to keep pushing.

This is the risk investors are now starting to price more carefully. Today’s shortage can become tomorrow’s balance. Tomorrow’s balance can become oversupply if capacity arrives faster than demand. The timing is uncertain, but the possibility matters.

Why the Market Still Likes SK Hynix

Even with those risks, it is easy to understand why traders continue to follow SK Hynix.

The company is in the right part of the semiconductor market. AI data centers need more memory. HBM remains one of the clearest bottlenecks in the system. Nvidia demand is still a powerful driver. And SK Hynix has already proven that it can convert this demand into very strong earnings.

That is not just hype. There is real business momentum behind the rally.

If AI infrastructure spending remains strong, SK Hynix could continue to benefit from premium products, high utilization and a better mix of HBM, server DRAM and enterprise SSDs. If HBM4 execution goes well, the company may be able to defend its leadership even as competition increases.

The stock also benefits from scarcity. There are not many large, liquid public companies with such direct exposure to the AI memory bottleneck. That makes SK Hynix an obvious target for investors looking beyond Nvidia.

So the bullish case is still alive. It is just no longer cheap or simple.

What Could Go Wrong

The main risk is expectations. After a stock has already moved hundreds of percent, investors do not just want good news. They want better-than-expected news. They want confidence that demand will stay strong, margins will remain high and competitors will not take too much share.

That is a high bar. SK Hynix could face pressure if Nvidia slows orders, if cloud AI spending cools, if Samsung or Micron gain share faster than expected, or if HBM supply expands enough to weaken pricing. The stock could also react badly if investors start to worry that Korea’s chip rally has become too concentrated.

There is also the broader semiconductor cycle. AI demand is powerful, but it does not make the industry immune to inventory, pricing and capex swings. When memory turns, it usually turns quickly.

That is why SK Hynix can be both a great company story and a risky stock at the same time. Those two things are not contradictory. They are often exactly what happens in crowded growth trades.

What Tapbit Users Should Know

SK Hynix has earned its place at the center of the AI memory trade. Its HBM leadership, Nvidia supply-chain role and record earnings have turned it into one of the most important AI infrastructure stocks in the world. The company is no longer just being valued as a cyclical memory producer. It is being valued as a critical supplier to the AI buildout.

That is the good news. The harder part is that the stock has already moved a long way.

Expectations are high. The trade is crowded. Samsung and Micron are chasing the same market. Nvidia is likely to keep using multiple suppliers. And memory, even when powered by AI demand, remains a cyclical business.

Users can visit Tapbit to explore supported crypto markets and educational resources. Existing users can log in, while new users can register here.

Frequently Asked Questions (FAQ)

What is SK Hynix?

SK Hynix is a major South Korean semiconductor company and one of the world’s leading memory chip makers. It produces DRAM, NAND, server memory, enterprise SSDs and high-bandwidth memory, also known as HBM.

Why is SK Hynix getting so much attention?

SK Hynix is getting attention because it has become one of the clearest beneficiaries of the AI memory boom. As AI data centers require more advanced memory, demand for HBM has increased sharply, and SK Hynix is one of the key suppliers in this market.

What is HBM?

HBM stands for high-bandwidth memory. It is a type of advanced stacked memory used in high-performance computing and AI accelerators. HBM helps move large amounts of data quickly, which is essential for training and running large AI models.