The AI trade used to be simple: follow the GPUs.

For a long time, investors watched Nvidia, AMD, Broadcom, and the cloud companies buying every accelerator they could get. That still matters. But the market is starting to pay more attention to something less flashy and just as important: memory.

SK Hynix’s plan for a U.S. ADR listing is a good example. This is not a normal IPO story. SK Hynix is already listed in South Korea. A U.S. ADR would mainly make it easier for global investors to trade one of the most important companies in the AI memory supply chain.

The bigger question is not where the stock trades. It is why memory has suddenly become so important.

AI chips need more than compute

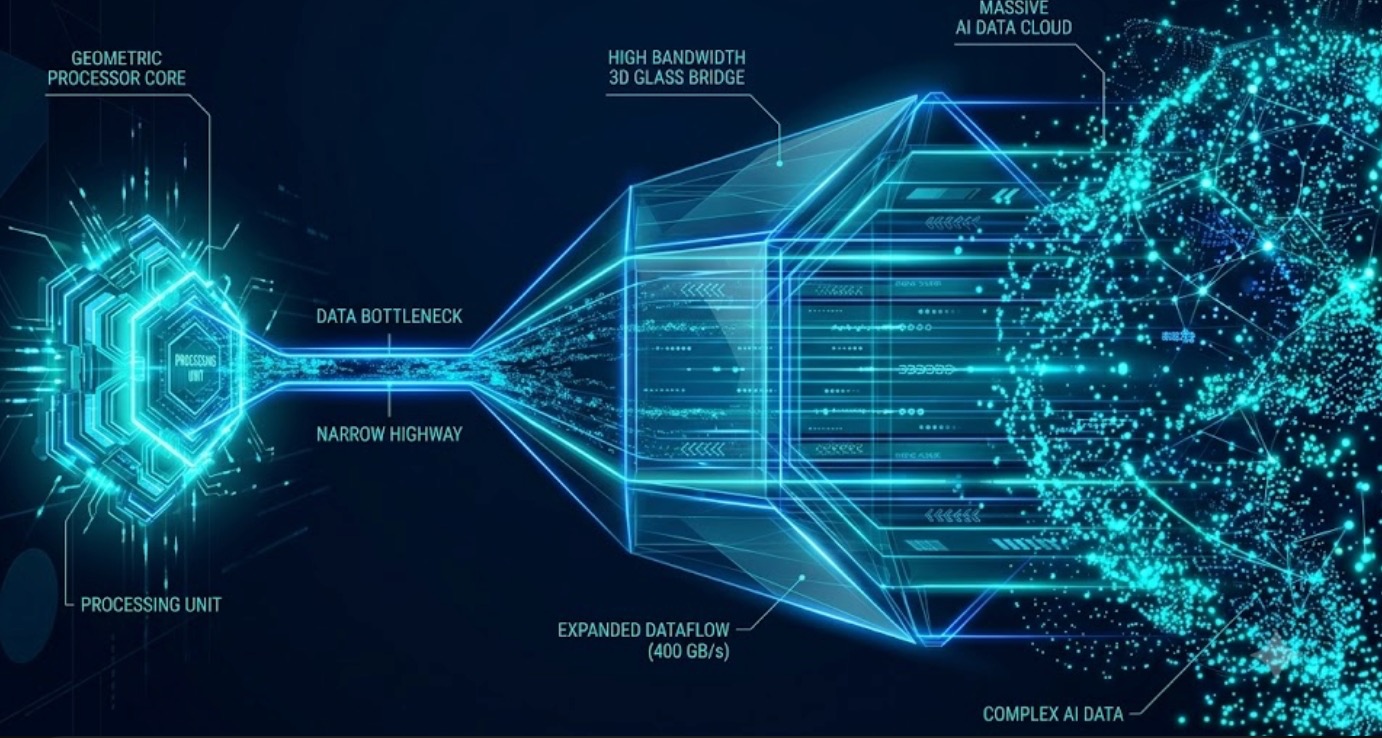

A powerful AI accelerator is not useful if it cannot move data fast enough.

That is why HBM, or high-bandwidth memory, has become such a key part of the AI hardware stack. HBM sits close to the processor and gives AI chips the bandwidth they need for large model training and inference.

This is not ordinary DRAM. It is harder to make, harder to package, and harder to scale. It also requires advanced manufacturing and testing capacity. That is why supply cannot catch up overnight.

As AI models get larger and data-center spending keeps rising, memory is no longer just a background component. It is becoming one of the main constraints on how quickly AI infrastructure can expand.

Why SK Hynix is getting more attention

SK Hynix is one of the leading suppliers of HBM, and that position matters more now than it did in previous memory cycles.

In the past, memory companies were usually treated as cyclical stocks. Demand would rise, supply would catch up, prices would fall, and the cycle would repeat. Investors knew the pattern.

This cycle feels different because HBM is tied directly to AI infrastructure spending. The customers are not just PC or smartphone makers. They are cloud giants, AI chipmakers, and data-center operators trying to secure supply years in advance.

That changes the way the market looks at memory leaders. SK Hynix is no longer just another DRAM company in a recovery cycle. It is one of the companies sitting near the center of the AI supply chain.

More money is flowing into memory

The reason memory companies need capital is straightforward: advanced chips are expensive to build.

HBM capacity requires specialized production lines, advanced packaging, testing, equipment, and process upgrades. New fabs take years. Yields take time to improve. Customers also need to qualify new products before volume shipments can ramp.

So even when companies announce expansion plans, supply does not arrive immediately.

That is important for traders. AI demand can move quickly, but semiconductor supply moves slowly. If HBM remains tight, pricing power may stay with the leading suppliers for longer than expected.

China is also trying to close the gap

This is not only a Korean or U.S. market story.

Chinese memory companies are also looking for capital and capacity. CXMT is pushing deeper into DRAM, while other chip firms are trying to use domestic listing channels to fund expansion and research.

The motivation is clear. AI has made memory a strategic supply-chain asset. Countries do not want to depend fully on overseas suppliers for the hardware behind AI computing.

That does not mean Chinese memory makers can immediately match SK Hynix, Samsung, or Micron at the high end of HBM. The technology gap is still real, and export controls remain a major factor.

But the direction is clear: memory is becoming a national infrastructure race, not just a corporate capex cycle.

The risk is that the market gets ahead of itself

The bullish case for memory is easy to see. AI demand is strong. HBM is tight. Leading suppliers have pricing power. Investors are looking for the next layer of the AI supply chain after GPUs.

But memory is still memory.

This industry has a history of overbuilding when times are good. If too much capacity comes online later, supply can swing from shortage to surplus. If AI capex slows, demand expectations can reset quickly. If next-generation HBM ramps faster than expected, older capacity may lose value sooner.

There is also geopolitical risk. Advanced memory depends on high-end equipment, packaging technology, export approvals, and global customers. Any change in trade restrictions or investment reviews can affect the supply chain.

So the theme is real, but it is not risk-free.

Tapbit View

SK Hynix’s U.S. listing plan is not just a stock-market event. It is a reminder that the AI supply chain is changing.

GPUs still get the headlines, but memory is becoming one of the real pressure points. HBM is hard to produce, demand is strong, and new capacity takes time. That gives leading memory companies a stronger role in the AI cycle.

For crypto traders, this is worth watching because AI-related tokens and compute narratives are ultimately tied to real hardware costs. If memory stays expensive, AI infrastructure stays expensive too.

The main takeaway is simple: the AI trade is moving beyond chips alone. Memory is now part of the center of the story.

HBM demand is real. SK Hynix is one of the key players. China is trying to catch up. But this is still a semiconductor cycle, and cycles can turn. The opportunity is there, but timing and valuation still matter.

Traders can follow more market updates on Tapbit, log in, or register to stay connected with global market opportunities.

Frequently Asked Questions (FAQ)

Why is SK Hynix’s U.S. listing plan getting attention?

Because SK Hynix is one of the key HBM suppliers in the AI hardware supply chain. A U.S. ADR listing would make it easier for global investors to trade exposure to one of the main beneficiaries of AI memory demand.

Is this the same as a traditional IPO?

No. SK Hynix is already listed in South Korea. The U.S. plan is better understood as an ADR listing, not a classic first-time IPO. The main point is broader investor access, not a brand-new company coming to market.

What is HBM?

HBM stands for high-bandwidth memory. It is advanced memory used close to AI processors to move large amounts of data quickly. AI accelerators need HBM because compute power alone is not enough if memory bandwidth becomes a bottleneck.