Apple has a way of making investors uncomfortable for the right reasons.

It is one of the strongest companies in the world. It has a massive user base, a sticky ecosystem, a high-margin services business, and a balance sheet most companies can only dream of. Yet when AAPL trades close to $300, the question becomes harder. Not because Apple is suddenly weak, but because a great company can still be a difficult buy when expectations are already high.

That is the situation traders are facing now.

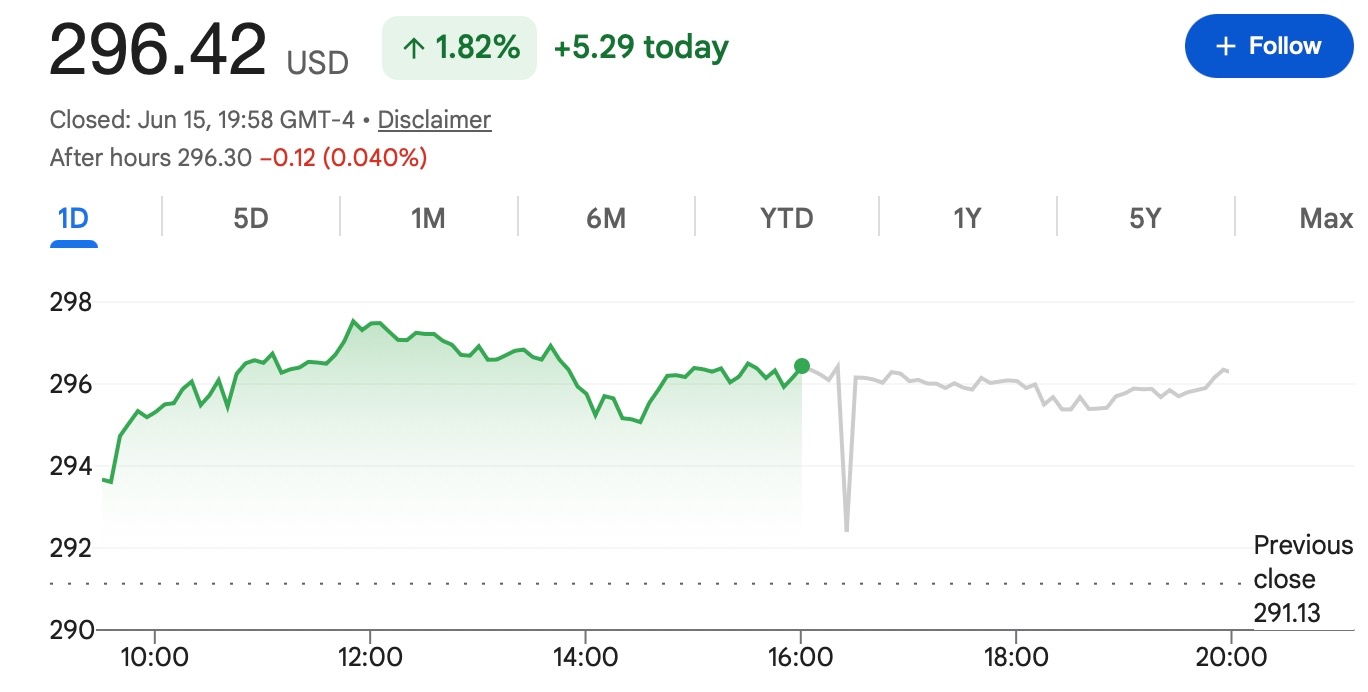

AAPL is sitting near the upper end of its 52-week range, close to a level that has both psychological and technical importance. The market is not debating whether Apple is a real business or whether its brand still matters. It is debating whether the next phase of growth — especially around AI and the iPhone upgrade cycle — is strong enough to justify paying a premium price today.

For Tapbit users tracking AAPL-USDT futures, that distinction matters. Being bullish on Apple as a company is not the same as having a clean trade setup.

Apple Is Strong, But the Stock Is No Longer Cheap

Apple’s latest numbers still give bulls plenty to work with. Revenue growth remains solid, iPhone sales are still central to the story, and services continue to give the company a more recurring revenue base than a traditional hardware maker.

That services business is one of the reasons investors keep giving Apple a premium valuation. iPhones, Macs, iPads, and wearables bring users into the ecosystem, but services keep them there. App Store spending, subscriptions, payments, cloud storage, and other platform revenue help make Apple less dependent on a single product launch.

Still, price matters. Around the $300 area, AAPL is not trading like an ignored value stock. It is trading like a company investors already believe in. That means the stock may need more than “Apple is a great company” to keep moving higher. It may need proof that AI features can drive upgrades, that services can keep expanding, and that margins can stay strong even if the broader consumer environment becomes less friendly.

This is where the trade gets more complicated. Apple does not need bad news to pull back. At this valuation, it may only need news that is not good enough.

The AI Story Is the Main Swing Factor

Apple’s AI strategy is now one of the biggest variables for AAPL. The bullish case is easy to understand. If Apple Intelligence and the new Siri experience become genuinely useful, they could give users a reason to upgrade older iPhones. Apple does not need every customer to rush into a new device at once. With a user base this large, even a moderate improvement in replacement demand can matter.

That is why investors are watching the AI rollout so closely. Apple is not trying to win the AI race the same way a cloud company or chipmaker might. Its advantage is distribution. If AI becomes deeply integrated into the iPhone, Mac, iPad, and Apple services ecosystem, Apple can turn software upgrades into hardware demand and long-term platform loyalty.

But the cautious view also deserves attention.

Apple has moved more slowly than some competitors in AI. Some investors are still waiting to see whether its features are compelling enough to change consumer behavior. A smarter Siri is helpful, but the market wants to know whether it is powerful enough to push people into a new iPhone cycle.

That is why the next few quarters matter. The announcement phase is mostly done. The proof phase is what comes next.

The $300 Level Is the Line Traders Are Watching

For short-term traders, AAPL is close to an important decision zone.

If the stock can break above $300 and hold there with strong volume, it could attract more momentum buyers. In that case, traders may start looking toward the previous high area and potentially higher targets if earnings support the move.

But if Apple struggles around $300, the setup changes. Failed breakouts near major psychological levels can lead to quick profit-taking, especially when a stock has already had a strong run. In that case, the $270 to $280 zone may become more interesting for buyers waiting for a better entry.

That does not mean AAPL must fall before it becomes attractive. It means the trade needs a plan. Buying blindly near resistance is different from buying a confirmed breakout or building slowly on weakness.

For long-term investors, dollar-cost averaging may still make sense. Apple is the kind of company many investors prefer to accumulate over time rather than trade around every headline. But even long-term buyers should think about position size, entry pace, and how much optimism is already reflected in the stock.

What This Means for AAPL-USDT Traders on Tapbit

AAPL-USDT futures give Tapbit users a way to trade Apple-linked price exposure, but they are not the same as owning Apple shares.

That point is important. A futures position can move quickly. Leverage can increase gains, but it can also turn a normal stock pullback into a much larger loss for the trader. Apple may be a high-quality company, but that does not make every leveraged long position safe.

Before trading AAPL-USDT, traders should be clear about the setup they are actually taking.

A breakout trader may wait for AAPL to move above $300 and hold that level. A pullback trader may prefer to see price return toward support before entering. A news-driven trader may focus on earnings, AI updates, product events, or analyst revisions.

The mistake is entering just because the Apple name feels safe. A safe company and a safe trade are not the same thing.

What Could Go Wrong?

The main risk is not that Apple suddenly becomes a bad company. The more realistic risk is that expectations are too high.

If AI adoption looks slow, if iPhone upgrades disappoint, or if services growth starts to cool, investors may question whether AAPL deserves such a rich valuation. A broader tech selloff could also pressure the stock, even if Apple’s own business remains healthy.

There is also the simple risk of crowded positioning. Apple is widely owned, widely followed, and deeply embedded in major indexes. When sentiment turns, large-cap leaders can become a source of liquidity for investors looking to reduce exposure.

For futures traders, this matters even more. A 3% or 5% move in the underlying stock may not sound dramatic, but with leverage it can be painful.

Bottom Line

Apple remains one of the highest-quality companies in the market. Its ecosystem is powerful, its services business is still valuable, and its AI roadmap gives investors a reason to stay interested.

But near $300, AAPL is not a low-expectation trade. The stock is already pricing in a strong future. To move meaningfully higher, Apple may need to prove that AI can do more than improve the user experience. It needs to show that AI can support a new upgrade cycle and strengthen earnings growth.

For investors, Apple can still be a long-term holding. For traders, the better approach is to respect the levels, wait for confirmation, and avoid chasing simply because the company is familiar.

For Tapbit users trading AAPL-USDT futures, the key takeaway is simple: Apple may be a great company, but leverage still needs discipline.

Traders can follow more market updates on Tapbit, log in, or register to stay connected with global market opportunities.

Frequently Asked Questions (FAQ)

Is Apple stock still a good buy near $300?

Apple remains a high-quality company, but near $300 the stock is no longer an obvious bargain. At this level, investors are already pricing in a strong business outlook, continued services growth, and optimism around Apple’s AI roadmap. For traders, the better approach may be to wait for either a confirmed breakout above $300 or a cleaner pullback entry.

Why is the $300 level important for AAPL?

The $300 area is both a psychological level and a technical zone many traders are watching. If AAPL breaks above it and holds, the move could attract momentum buyers. If the stock fails near that level, it may signal that buyers are not ready to push the price higher yet.

What could drive Apple stock higher from here?

A stronger iPhone upgrade cycle, better-than-expected services revenue, positive AI adoption, and a supportive Nasdaq environment could all help AAPL move higher. The market especially wants to see whether Apple Intelligence and the new Siri experience can create real demand for newer devices.