For most of the AI boom, investors focused on GPUs.

That made sense. Without high-end accelerators, the AI buildout would not exist. But in 2026, the market has started to pay attention to another bottleneck: memory.

AI servers do not only need compute. They need DRAM, HBM, NAND, enterprise SSDs, and fast storage systems that can keep up with training and inference workloads. That shift has turned memory chips from a cyclical hardware category into one of the most important supply-chain trades in the AI era.

SanDisk and Micron are now at the center of that repricing. SanDisk has become the high-beta NAND story. Micron has become the broader DRAM, NAND, and HBM story. Both have delivered huge gains. Both have strong data behind the move. And both now trade with enough momentum that traders need to separate the industry story from the entry price.

SanDisk Is No Longer Just a Storage Name

SanDisk’s rally has been extreme, but it is not based on hype alone.

Recent market data shows SanDisk trading around $2,184.75, with an intraday high near $2,218.60 and a market capitalization of roughly $343 billion. That comes after the stock had already surged more than 700% year to date, according to the earlier market snapshot.

The financials explain why traders have been willing to chase the move.

For fiscal Q3 2026, SanDisk reported revenue of $5.95 billion, up 97% sequentially and above its guidance range. GAAP net income reached $3.615 billion, with diluted EPS of $23.03. The company said the outperformance was driven by stronger pricing and a mix shift toward higher-value customers, with the datacenter business up 233% sequentially.

That is the key number. SanDisk is not being revalued because consumers suddenly want more USB drives or retail SSDs. It is being revalued because AI data centers are absorbing high-performance NAND and enterprise SSD capacity at a pace the market did not fully price in.

This is why the stock has traded more like an AI infrastructure supplier than a traditional storage company.

Why Pure NAND Exposure Matters

SanDisk’s business structure gives it a different kind of earnings sensitivity from Micron.

After becoming a more focused NAND player, SanDisk is more directly exposed to NAND pricing and enterprise SSD demand. When NAND supply tightens and data center demand accelerates, that focus becomes powerful.

A traditional server already needs storage. An AI server needs much more. Earlier industry estimates suggest a single AI server can use more than three times the NAND flash of a traditional server. As AI workloads shift from model training to inference, storage demand does not disappear. Inference workloads still need low latency, high concurrency, fast access, and large-scale data movement.

That is why NAND is starting to look less like a commodity input and more like a strategic constraint.

When supply is tight, a pure NAND player has more direct upside. That is exactly what the market has been pricing into SanDisk.

Long-Term Deals Are Changing the Memory Business

The most important part of the SanDisk story may not be the stock price.

It may be the contract structure. SanDisk has signed multiple long-term supply agreements under its new business model. Public reports indicate that more than one-third of its fiscal 2027 bit supply has already been locked under five long-term agreements. The first three contracts alone reportedly represent roughly $42 billion in minimum revenue commitments, supported by more than $11 billion in financial guarantees.

That is a major change for a memory company. Historically, memory chips were one of the most cyclical parts of the semiconductor market. Prices moved sharply with inventory cycles, and customers negotiated aggressively when supply loosened.

This cycle looks different. AI customers want guaranteed supply. Memory producers want visibility. Long-term contracts give both sides more certainty. For suppliers like SanDisk, that can reduce the old boom-bust pattern and support a higher valuation multiple.

This does not eliminate cyclicality. But it changes the discussion. The market is no longer asking only, “Where are NAND prices this quarter?” It is asking, “How much of future AI storage demand is already locked in?”

Micron Is the Broader Memory Trade

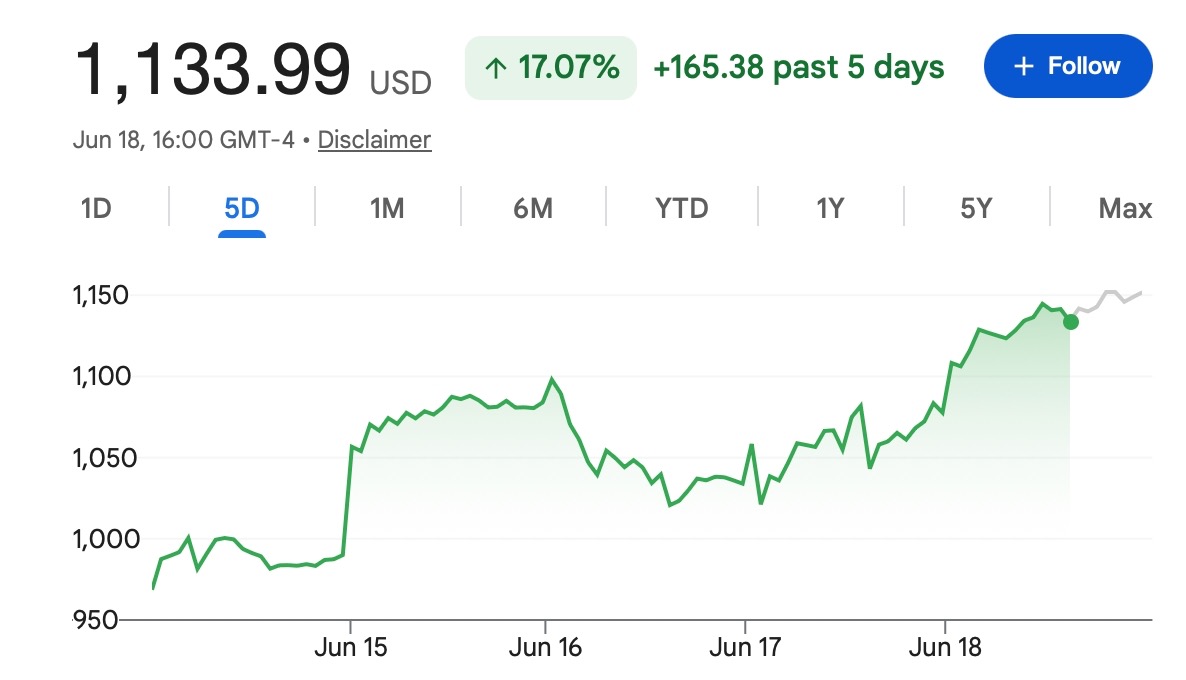

Micron’s rally has also been powerful, but the setup is different. Recent market data shows Micron trading around $1,133.99, with an intraday high near $1,154.69 and a market capitalization of about $1.295 trillion. The stock has also posted massive gains in 2026, supported by demand across DRAM, NAND, and HBM.

Micron is not a pure NAND trade. That is both a strength and a limitation. Its exposure to DRAM and HBM gives it a broader AI memory profile. HBM is critical for advanced AI accelerators, while DRAM demand is rising as AI servers require far more memory than traditional systems. Industry estimates suggest AI servers can use 8 to 10 times more DRAM than conventional servers.

That gives Micron several growth engines at once. The trade-off is that Micron may not have the same single-segment torque as SanDisk during a NAND shortage. Instead, it offers a more balanced memory cycle exposure: DRAM, NAND, HBM, enterprise storage, and AI server demand.

That is why some investors may view SanDisk as the higher-beta trade and Micron as the more diversified AI memory leader.

The Shortage Is Spreading Beyond Data Centers

The memory shortage is no longer just an issue for cloud companies.

It is starting to hit consumer hardware. Silicon Motion executives recently warned that NAND shortages could worsen into 2027 as AI data centers absorb more supply. One forecast suggested that 70% to 80% of NAND could be directed toward AI data centers by 2027, leaving less supply for PCs, smartphones, gaming systems, and retail SSDs.

That helps explain why consumer SSD availability has tightened and why retail storage markets are seeing pressure. It also shows how large the AI demand shift has become.

When AI data centers can absorb most of the available supply, memory producers gain pricing power. Downstream buyers either accept higher costs, sign longer contracts, or risk not getting enough supply.

For consumers, that can mean higher prices for laptops, desktops, phones, gaming PCs, and SSD upgrades. For memory companies, it means better margins and stronger negotiating power.

The Trade Is Real, But It Is Crowded

This is the part traders should not ignore. The industry story is strong. The price action is also stretched.

MarketWatch recently noted that both Micron and SanDisk are deeply overbought on technical indicators. Micron’s RSI was around 90.98, while SanDisk’s RSI was near 98.96. For context, an RSI above 70 is often considered overbought.

That does not mean the stocks must fall immediately. Strong stocks can stay overbought for longer than traders expect, especially when earnings estimates are being revised higher and institutions are chasing exposure.

But it does mean the easy part of the trade may already be priced in. SanDisk has rallied because NAND pricing, data center demand, and long-term contracts all improved at once. Micron has rallied because DRAM, NAND, and HBM are all tied to the AI buildout. Those are real drivers.

The risk is that everyone now knows the story. When a trade becomes crowded, even good news may not be enough. A small earnings miss, softer guidance, supply expansion, slower AI capex, or profit-taking after a vertical rally can trigger sharp pullbacks.

That is why traders should avoid treating “AI memory” as a risk-free theme.

Bottom Line

SanDisk and Micron are no longer side stories in the AI market.

SanDisk is being repriced as a pure NAND winner in a world where AI data centers are absorbing more enterprise SSD and flash storage supply. Its fiscal Q3 numbers — $5.95 billion in revenue, 97% sequential growth, $3.615 billion in GAAP net income, and 233% sequential datacenter growth — show that the story is backed by real operating leverage.

Micron is being repriced as the broader memory leader, with exposure to DRAM, NAND, and HBM. Its current market value above $1 trillion reflects how aggressively investors are now pricing AI server memory demand.

The memory supercycle is real. But the trade is crowded.

Explore the latest markets on Tapbit, log in to trade, or create an account to get started.

Frequently Asked Questions (FAQ)

Why are SanDisk and Micron getting so much attention in 2026?

SanDisk and Micron are being repriced because AI data centers need far more memory and storage than traditional servers. GPUs still get most of the attention, but AI workloads also require large amounts of DRAM, HBM, NAND, and enterprise SSD capacity.

Is SanDisk’s rally only driven by AI hype?

No. The rally has been supported by real operating data. SanDisk reported strong revenue growth, higher profitability, and sharp datacenter demand growth in fiscal Q3 2026. The market is reacting to both AI demand and improved pricing power in NAND.

Why is SanDisk considered a high-beta NAND trade?

SanDisk has more direct exposure to NAND flash and enterprise SSD demand. When NAND supply is tight and AI data centers are buying aggressively, a focused NAND company can see stronger profit elasticity than a more diversified memory business.hhh