Qualcomm is back on traders’ radar.

After spending much of the past few years tied closely to the smartphone cycle, QCOM is now being discussed in a broader context: AI phones, automotive chips, connected devices, edge computing and even custom silicon opportunities beyond mobile. That does not mean the stock has a clear path back to its previous highs. But it does make the $250 question worth revisiting.

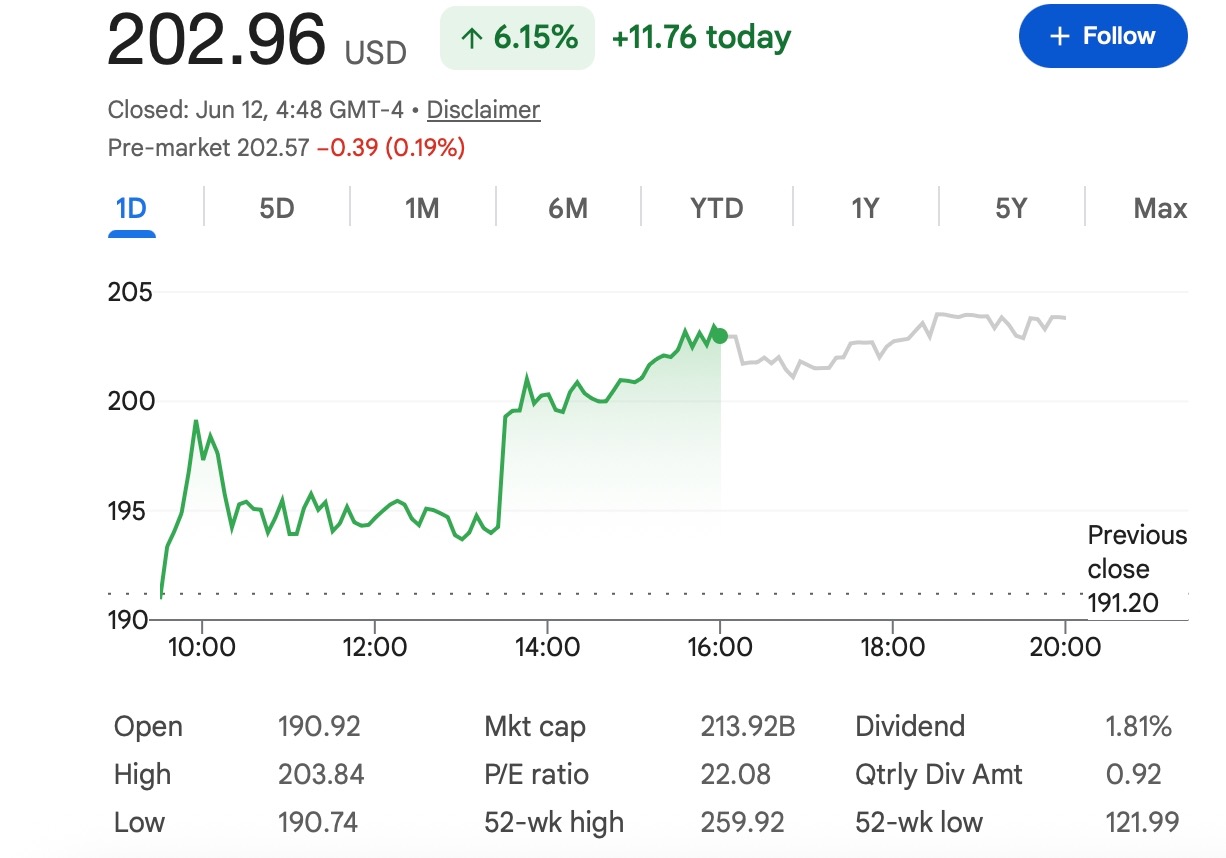

At a recent reference price of around $203, QCOM would need to gain roughly 23% to reach $250. That is a meaningful move for a large-cap semiconductor stock, but not an unrealistic one if earnings expectations improve and chip-sector sentiment stays firm.

The more important question is not whether QCOM can touch $250 in theory. It is what needs to happen for investors to believe that level is justified.

Qualcomm Is Trying to Move Beyond the Smartphone Label

Qualcomm is still best known for Snapdragon processors, modem chips and wireless technology used in smartphones. That part of the business remains important, and it is still one of the biggest reasons investors watch the stock.

But the company is no longer just a handset-cycle story. The market is paying closer attention to Qualcomm’s role in AI-enabled devices, connected vehicles and low-power computing. These are areas where the company already has technical advantages: efficient chips, strong wireless connectivity, on-device processing and deep relationships with major hardware makers.

That shift matters because valuation depends on how investors define the company. If QCOM is seen mainly as a smartphone supplier, its multiple may stay tied to handset demand. If it is increasingly viewed as a broader AI and connected-computing platform company, the market may be willing to price in more upside.

Why AI Smartphones Matter

AI phones are one of the clearest potential catalysts for Qualcomm.

On-device AI requires more capable processors, stronger NPUs, better power efficiency and faster connectivity. These are all areas where Qualcomm has spent years building expertise. If phone makers can turn AI features into a real reason for consumers to upgrade, Qualcomm could benefit from stronger demand for premium Snapdragon platforms.

That said, this is still an early story. The market has heard a lot about AI phones, but investors will need to see real evidence: better shipment numbers, stronger OEM demand, healthier guidance and signs that AI features are actually influencing consumer behavior.

In other words, AI smartphones are a credible growth driver, but they are not yet a guaranteed upgrade cycle.

Automotive Chips Could Change the Narrative

The automotive business may be even more important for Qualcomm’s long-term story.

Cars are becoming more connected, more software-driven and more dependent on advanced computing platforms. Digital cockpits, in-car connectivity, driver-assistance systems and infotainment all create opportunities for chipmakers with strong processing and wireless capabilities.

Qualcomm has already built a meaningful automotive pipeline, and this business gives investors something they do not always get from smartphones: longer product cycles and better revenue visibility. Once a chip platform is designed into a vehicle program, it can support revenue over several years.

If automotive revenue keeps scaling, QCOM may gradually become less exposed to the ups and downs of phone replacement cycles. That would be one of the stronger arguments for a higher valuation.

Licensing Still Provides a Profit Anchor

Qualcomm’s licensing business is another reason the stock remains different from many hardware-focused chip names.

Patent licensing has historically supported strong margins and cash flow. When the chip business is recovering, stable licensing revenue can make the company’s earnings profile look more resilient.

This does not remove risk. Licensing can still face regulatory pressure, customer negotiations and legal disputes. But as long as the business remains stable, it gives Qualcomm an important profit base while newer growth areas develop.

What Could Push QCOM Toward $250?

A move toward $250 would likely require several things to happen together.

First, the smartphone business needs to improve. Qualcomm does not need a massive global phone boom, but it does need signs that premium Android demand is healthy and that AI features are helping the replacement cycle.

Second, automotive growth needs to remain visible. Investors will want evidence that design wins are turning into revenue and that Qualcomm can keep expanding its role inside connected vehicles.

Third, the broader semiconductor market needs to stay supportive. QCOM does not trade in isolation. If chip stocks are rising on AI demand, stronger earnings and improved risk appetite, Qualcomm has a better chance of participating in that move.

Finally, analyst expectations may need to move higher. Current target-price ranges still show disagreement around Qualcomm’s fair value. For $250 to become a more widely accepted level, the market will likely need stronger earnings revisions and clearer confidence in future growth.

What Could Keep the Stock Below $250?

The main risk is still smartphones.

If Android demand weakens, consumers delay upgrades or handset makers cut orders, QCOM’s near-term revenue outlook could come under pressure. AI features may help, but they will not fully offset a weak phone cycle unless users actually buy new devices.

Competition is another issue. Qualcomm faces pressure from rival chipmakers, customer in-house chip efforts and supply-chain diversification. Even strong products can face margin pressure if customers push for lower prices or alternative suppliers.

There is also the broader market risk. Semiconductor stocks can move sharply when interest-rate expectations, AI sentiment or technology valuations change. A stock can have a solid company story and still struggle if the whole sector de-rates.

A Reasonable 2026 View

The most balanced view is that $250 is possible, but it is not the default outcome.

If AI phone demand improves, automotive revenue keeps growing and semiconductor sentiment remains strong, QCOM could move into the $230–$250 range and potentially test $250. That would be the constructive case.

If results are steady but not especially strong, the stock may spend more time in a wide range between the high $100s and low $200s while investors wait for clearer proof of growth.

If smartphone demand disappoints or chip valuations pull back, QCOM could remain below $250 even if its long-term strategy remains intact.

Tapbit Academy Takeaway

Qualcomm has a credible path back to $250, but the stock still needs confirmation from the business.

The company sits at the intersection of several major themes: AI devices, automotive computing, wireless connectivity and semiconductor recovery. That gives QCOM a stronger long-term story than a simple handset rebound.

At the same time, investors should not ignore the risks. Mobile demand still matters, competition is real and valuation depends heavily on market sentiment toward chip stocks.

For traders and market watchers, the key signals to follow are upcoming earnings, smartphone demand trends, automotive revenue growth, AI phone adoption and any change in analyst expectations.

QCOM does not need a perfect environment to move higher. But to make $250 look sustainable, Qualcomm will need to show that its growth story is becoming broader, more durable and less dependent on the smartphone cycle alone.

Traders can follow more market updates on Tapbit, log in, or register to stay connected with global market opportunities.

Frequently Asked Questions (FAQ)

Can QCOM reach $250 in 2026?

QCOM can reach $250 in 2026, but it would likely require stronger earnings confidence, healthier smartphone demand, continued automotive chip growth and supportive sentiment across the semiconductor sector. At a recent reference price of around $203, the stock would need to gain roughly 23% to reach $250.

Is $250 a realistic target for Qualcomm stock?

$250 is realistic as an optimistic scenario, but it should not be treated as the base case. Qualcomm has the right exposure to AI smartphones, connected vehicles and wireless technology, but the market still needs clearer evidence that these growth drivers can support a higher valuation.

What could push Qualcomm stock higher?

The main upside drivers include stronger premium Android demand, wider adoption of AI smartphones, growth in automotive chips, stable licensing revenue and a broader rally in semiconductor stocks. Positive earnings revisions and stronger management guidance could also help.