Palantir is no longer a stock that needs to convince the market it has an AI angle. That part is done.

The harder question now is whether the company can keep growing fast enough to justify how much investors are already paying for that story.

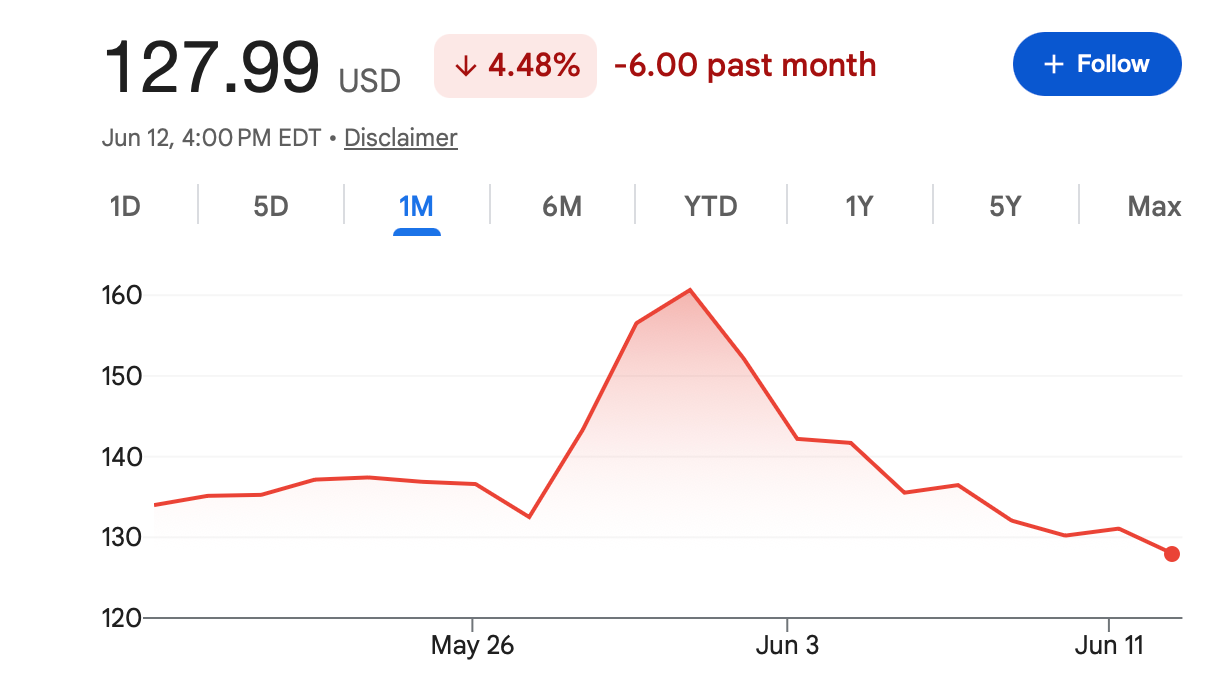

That is what makes the $255 target interesting. With PLTR recently trading near the high-$120s, a move to $255 would mean the stock almost doubles from current levels. For a company that has already had a powerful run, that is not a small ask.

It is possible. But it is not the kind of target that happens just because “AI is hot.” Palantir would need to keep delivering very strong numbers, prove that AIP adoption is turning into durable revenue, and benefit from a market that remains willing to pay premium prices for high-growth AI names.

In short, $255 is a bull case — not a base case.

Palantir Has Earned the Market’s Attention

The reason PLTR keeps attracting buyers is simple: the company is showing real momentum.

Palantir’s latest results were strong, especially in the U.S. commercial business. For years, the company was mainly viewed through the lens of government contracts and defense-related data platforms. That business still matters, but it is no longer the whole story.

The market is now focused on AIP, Palantir’s Artificial Intelligence Platform. The excitement around AIP is not only about branding. Investors want to know whether Palantir can become a core layer for companies trying to use AI inside their daily operations.

That is an important distinction.

A lot of companies can talk about AI. Fewer can show that customers are actually deploying it, paying for it, and expanding usage over time. Palantir’s bull case rests on the idea that it belongs in the second group.

If AIP keeps moving from pilot projects to larger enterprise rollouts, the market may continue to treat Palantir as one of the cleaner ways to trade applied AI.

Why $255 Is Still a Stretch

The path to $255 is not impossible, but it does require a lot to go right.

Palantir needs to keep showing that commercial demand is not just a short-term burst of AI enthusiasm. Revenue growth has to stay strong, customer expansion has to continue, and management needs to keep giving the market confidence that the current momentum can last.

Margins also matter. PLTR is not being valued like an early-stage software company that can ignore profitability. Investors are already pricing in a business that can grow quickly and convert that growth into strong cash flow. If margins improve while revenue keeps accelerating, the stock can keep its premium multiple. If not, the market may become less forgiving.

Then there is the macro backdrop. PLTR is still a high-multiple growth stock. These stocks usually perform best when investors are comfortable taking risk and when interest-rate expectations are not moving sharply higher. If the broader market turns defensive, even strong AI names can struggle.

That is the key point: Palantir can execute well and still see its stock pressured if the market decides that valuations across AI have run too far.

The Valuation Debate Is the Real Fight

The debate around PLTR is not really about whether Palantir is a good company. Most investors now accept that the business is in a much stronger position than it was a few years ago.

The debate is about price.

At current valuation levels, Palantir has very little room for ordinary results. Good may not be good enough. The company probably needs to keep producing the kind of earnings reports that make analysts raise estimates rather than simply confirm them.

That is why the stock can be so sensitive around earnings. A small miss in guidance, slower commercial growth, or any sign that AIP adoption is taking longer to scale could trigger a sharp reaction. The higher the valuation, the more fragile the setup becomes.

This does not break the bull case. It just means the bull case has to keep being proven.

AI Momentum Is Helping, but It Can Also Turn

Right now, Palantir benefits from one of the strongest themes in global markets: enterprise AI.

Investors are looking for companies that can turn AI from a concept into real business outcomes. Palantir fits that narrative better than many software names because its products are built around data integration, decision-making and operational use cases. That gives the company a clearer commercial story than firms that are simply adding AI features to existing tools.

But AI is also a crowded trade. When a theme becomes this popular, the market starts to separate companies that are actually monetizing it from those that are only talking about it. Palantir has been on the right side of that divide so far. The risk is that expectations keep rising faster than even a strong business can meet.

That is usually where volatility appears.

What Would Make the $255 Case More Convincing?

For PLTR to make a serious move toward $255, investors would likely need to see a few things over the next several quarters.

The first is continued strength in U.S. commercial revenue. This is the part of the business that can change the market’s view of Palantir most quickly. If commercial growth keeps surprising to the upside, the stock’s premium becomes easier to defend.

The second is evidence that AIP deals are scaling. Pilot activity is useful, but large deployments are what matter. Investors will watch customer growth, contract size, remaining performance obligations and management commentary for signs that demand is becoming more durable.

The third is margin discipline. If Palantir can grow quickly without giving up profitability, it strengthens the argument that the company deserves to trade at a premium to most software peers.

The fourth is market sentiment. A risk-on market would help. A higher-rate, risk-off market would make the $255 path much harder.

For Traders, This Is Not a Simple Chase

PLTR is the kind of stock that can punish both sides.

Short sellers have been hurt by the company’s momentum and improving fundamentals. But late buyers can also get caught if expectations become too stretched before earnings or macro conditions change.

For traders using PLTR-linked products, the main point is to separate the company story from the trade setup. Palantir may remain one of the best-known AI names in the market, but that does not mean every entry point offers attractive risk-reward.

Earnings dates, analyst revisions, AI-sector sentiment and broader rate expectations can all move the stock quickly. Around those events, position sizing matters more than conviction.

Bottom Line

PLTR reaching $255 in 2026 is not impossible. The company has the AI momentum, the commercial traction and the market attention needed to keep the bull case alive.

But the bar is high.

At this valuation, Palantir cannot simply be good. It needs to keep looking exceptional. The market needs to see that AIP is not just driving excitement, but turning into large, repeatable and profitable enterprise demand.

If that happens, $255 becomes a serious conversation. If growth slows, margins disappoint, or investors rotate out of high-multiple AI stocks, the same valuation that supports the upside case could quickly become the biggest risk.

For now, PLTR remains one of the most important names in the applied AI trade. The opportunity is real. So is the pressure to keep proving it.

Traders can follow more market updates on Tapbit, log in, or register to stay connected with global market opportunities.

Frequently Asked Questions (FAQ)

Can PLTR really reach $255 in 2026?

It is possible, but it should be viewed as a bull-case scenario rather than a base-case forecast. For PLTR to reach $255, Palantir would need to keep delivering strong revenue growth, show continued adoption of AIP, maintain healthy margins and benefit from a market that remains supportive of high-growth AI stocks.

Why is $255 such an important level?

The $255 level implies that PLTR would nearly double from its recent trading range. That makes it a useful way to frame the upside case, but it also shows how much growth and investor confidence would be needed to justify that move.

What is the main reason investors are bullish on Palantir?

The main bullish argument is AIP, Palantir’s Artificial Intelligence Platform. Investors believe AIP could help Palantir move beyond its government-focused image and become a major enterprise AI software provider. If more companies move from small pilots to large deployments, the bull case becomes stronger.