Seamos honestos: los préstamos de criptomonedas obtuvieron una terrible reputación después del colapso de CeFi en 2022. Las empresas tomaron depósitos minoristas, los jugaron a puerta cerrada y finalmente quebraron, dejando a los usuarios sin nada.

Pero mientras los prestamistas centralizados congelaban los retiros, los protocolos descentralizados como Aave no perdieron el ritmo. ¿Por qué? Porque el código no miente y no entra en pánico.

Si está conservando activos a largo plazo, tener criptomonedas inactivas es dejar dinero sobre la mesa. Aquí hay un desglose práctico de cómo funciona Aave, por qué sobrevivió al mercado bajista y cómo puede usarlo para exprimir más utilidad de su cartera.

CeFi vs. DeFi: Por qué Aave Ganó

La diferencia entre un prestamista de criptomonedas en quiebra y Aave se reduce a una cosa: la transparencia.

-

Sin Cajas Negras: Los prestamistas centralizados operaban como bancos tradicionales pero con cero supervisión. Aave se ejecuta completamente en contratos inteligentes de código abierto en Ethereum (y Layer-2s como Arbitrum o Base). Puede verificar cada dólar en los pools de liquidez en cadena, 24/7.

-

Acceso sin Permiso: No hay verificaciones de crédito. No hay gerentes de cuenta. No hay bloqueo geográfico. Su billetera Web3 (como MetaMask) es su única identidad.

-

Gestión de Riesgos Brutal: A Aave no le importa quién eres. Si el colateral de un prestatario cae por debajo de un umbral codificado, el protocolo lo liquida automáticamente para proteger a los prestamistas. No hay rescates ni CEO que pause el comercio.

Cómo Funcionan Realmente los Pools de Liquidez

En lugar de que un banco empareje a un prestamista específico con un prestatario específico, Aave utiliza pools de liquidez peer-to-peer.

-

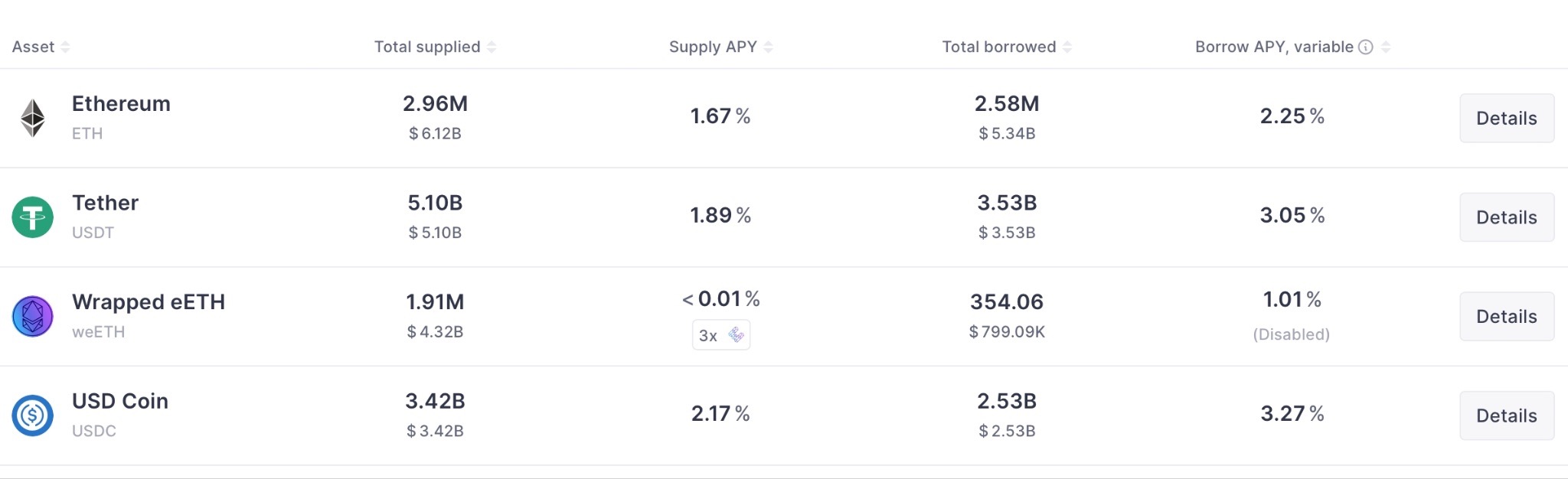

Prestar (Suministrar): Usted deposita activos como USDC, ETH o WBTC en un contrato inteligente. El protocolo le paga un Rendimiento Porcentual Anual (APY) dinámico basado en la demanda de préstamos en tiempo real. Ese interés se capitaliza continuamente con cada bloque de la cadena de bloques.

-

Pedir Prestado: Digamos que desea efectivo para comprar una caída del mercado, pero se niega a vender su ETH. Puede depositar su ETH en Aave como colateral y pedir prestado stablecoins contra él. Usted paga una tasa de interés flotante o fija a los proveedores.

-

Préstamos Flash: Esto es principalmente para desarrolladores, pero es lo que hizo famoso a Aave. Puede pedir prestado millones de dólares sin colateral, siempre que devuelva el préstamo y la tarifa dentro del mismo bloque de transacción de la cadena de bloques. Se utiliza mucho para arbitraje rápido.

Poniéndolo en Práctica: Tapbit + Aave

Usar un exchange centralizado junto con DeFi es el plan exacto que usan los profesionales para maximizar su eficiencia de capital. Aquí se explica cómo ejecutar el flujo de trabajo, paso a paso, sin arruinarse por las tarifas o cometer errores de novato:

Paso 1: Acumule sus Activos (y No Olvide el Dinero para el Gas)

Antes de siquiera mirar Aave, necesita tener los tokens correctos en su cuenta. En realidad, necesita dos cosas diferentes: el activo que desea prestar (como USDC, USDT o su reserva de ETH a largo plazo) y el token nativo "gas" para pagar las tarifas de transacción de la cadena de bloques.

Nada es más frustrante que enviar $5,000 en stablecoins a su MetaMask, solo para darse cuenta de que no puede depositarlo en Aave porque no tiene $5 en ETH para pagar la tarifa de la red.

Si su billetera está vacía, Regístrese en Tapbit para cargar. Compre sus activos principales y obtenga un poco del token de gas nativo. La liquidez en Tapbit es lo suficientemente profunda como para que no sufra un deslizamiento loco al construir su posición inicial.

Paso 2: Retire a Autocustodia (Elija su Red Sabiamente)

Aave no tiene sus fondos, su billetera Web3 (como MetaMask, Trust Wallet o Rabby) los tiene. Necesita retirar sus activos recién comprados de su billetera spot de Tapbit a su dirección personal. Si no sabe cómo retirar activos, puede consultar nuestro artículo ‘La Guía Completa para Retirar Criptomonedas (En Cadena y Transferencia Interna)‘

Aquí está la parte más crítica: Selección de Red. Aave se ejecuta en la Red Principal de Ethereum, pero las tarifas de gas de la red principal pueden agotar su rendimiento si no está moviendo una gran cantidad. Afortunadamente, Aave también opera en redes Layer-2 más rápidas y económicas como Arbitrum, Optimism y Polygon.

-

Decida qué red se adapta al tamaño de su capital.

-

Copie su dirección de MetaMask.

-

Vaya a la página de retiro de Tapbit, pegue su dirección y asegúrese de seleccionar exactamente la misma red (por ejemplo, retire su USDC a través de Arbitrum One, no ERC-20, para ahorrar en tarifas).

-

Consejo profesional: Siempre envíe una pequeña transacción de prueba de $10 si es la primera vez.

Paso 3: Conéctese a Aave y Apruebe

Diríjase a aave.com y haga clic en Conectar Billetera. Asegúrese de que el menú desplegable de red en la esquina superior derecha de Aave coincida con la red a la que acaba de enviar sus fondos (por ejemplo, cámbielo de Ethereum a Arbitrum). Antes de poder suministrar o pedir prestado, deberá firmar una transacción rápida en su billetera para "aprobar" que el contrato inteligente de Aave interactúe con sus tokens.

Paso 4: Ejecute el Bucle

Ahora está dentro. Haga clic en "Suministrar" en sus stablecoins para comenzar a ganar APY pasivo de inmediato. O, si desea desbloquear liquidez: suministre su ETH o WBTC a largo plazo como colateral, pida prestado stablecoins contra él y envíe esas stablecoins de regreso a su cuenta de exchange.

No Sea Liquidado: Entendiendo el LTV

Pedir prestado contra sus criptomonedas es increíblemente poderoso, pero también es la forma en que los traders descuidados arruinan sus cuentas. Tiene que prestar atención a su Relación Préstamo-Valor (LTV) y a su Umbral de Liquidación.

Si ETH tiene un LTV del 80%, depositar $10,000 en ETH le permite pedir prestado un máximo de $8,000 en otro activo. Pero si el mercado cae y el valor de su colateral cae por debajo del umbral de liquidación, los bots de Aave venderán forzosamente su ETH con una penalización (generalmente alrededor del 5%) para pagar su deuda.

La Regla de Oro: Nunca pida prestado el LTV máximo. Mantenga sus límites de préstamo conservadores, generalmente por debajo del 40% o 50%, para que pueda dormir tranquilo durante caídas repentinas del mercado sin preocuparse de que su colateral sea liquidado.

El Módulo de Seguridad (la Póliza de Seguro de Aave)

¿Qué sucede si el mercado se desploma tan rápido que las liquidaciones no cubren la deuda incobrable? Aave tiene un respaldo llamado Módulo de Seguridad.

Los usuarios pueden apostar el token nativo del protocolo, AAVE, en este módulo para obtener rendimiento. Si el protocolo alguna vez se vuelve insolvente, hasta el 30% de este AAVE apostado puede ser reducido y subastado para cubrir el déficit. Actúa como un fondo de seguro descentralizado que mantiene a los prestamistas íntegros.

Conclusión

Aave demostró que los préstamos descentralizados y sobrecolateralizados funcionan. Elimina la codicia humana que destruyó CeFi y la reemplaza con matemáticas implacables y transparentes. Si desea construir una cartera verdaderamente eficiente en capital, combinar el motor de trading de Tapbit con los rieles de crédito descentralizados de Aave es una de las mejores configuraciones que puede tener.

Preguntas Frecuentes (FAQ)

¿Necesito pasar KYC para usar Aave?

No. No hay cuentas ni verificaciones de antecedentes para usar el protocolo. La dirección de su billetera Web3 es su única identificación.

¿Cómo se deciden las tasas de interés de Aave?

Es puramente algorítmico y se basa en la utilización. Si mucha gente está pidiendo prestado USDC del pool, la tasa de interés de USDC aumenta automáticamente. Esto atrae a más prestamistas para suministrar USDC e incentiva a los prestatarios actuales a pagar sus préstamos.

¿Cuándo tengo que pagar mi préstamo de Aave?

A diferencia de una hipoteca bancaria tradicional, no hay una fecha de pago fija. Mientras el valor de su colateral se mantenga de forma segura por encima del umbral de liquidación, puede mantener el préstamo abierto para siempre. El interés simplemente seguirá sumándose a su deuda total con el tiempo.