SpaceX’s IPO did more than create one of the biggest public market stories of the year.

It also gave the tokenized stock market its first real stress test. Before SpaceX listed publicly, crypto-native products built around the company were mostly about access. Retail demand was high, but real SpaceX shares were difficult to reach. Tokenized products offered a way to follow the private-market story, even if the structure varied from one issuer to another.

That changed once SpaceX began trading publicly under the ticker SPCX.

Now there is a public stock price. There is a public market benchmark. There is daily volume. There are options, derivatives, tokenized versions, and crypto-native trading products all trying to reflect the same company in different ways. That is where things get interesting — and more complicated.

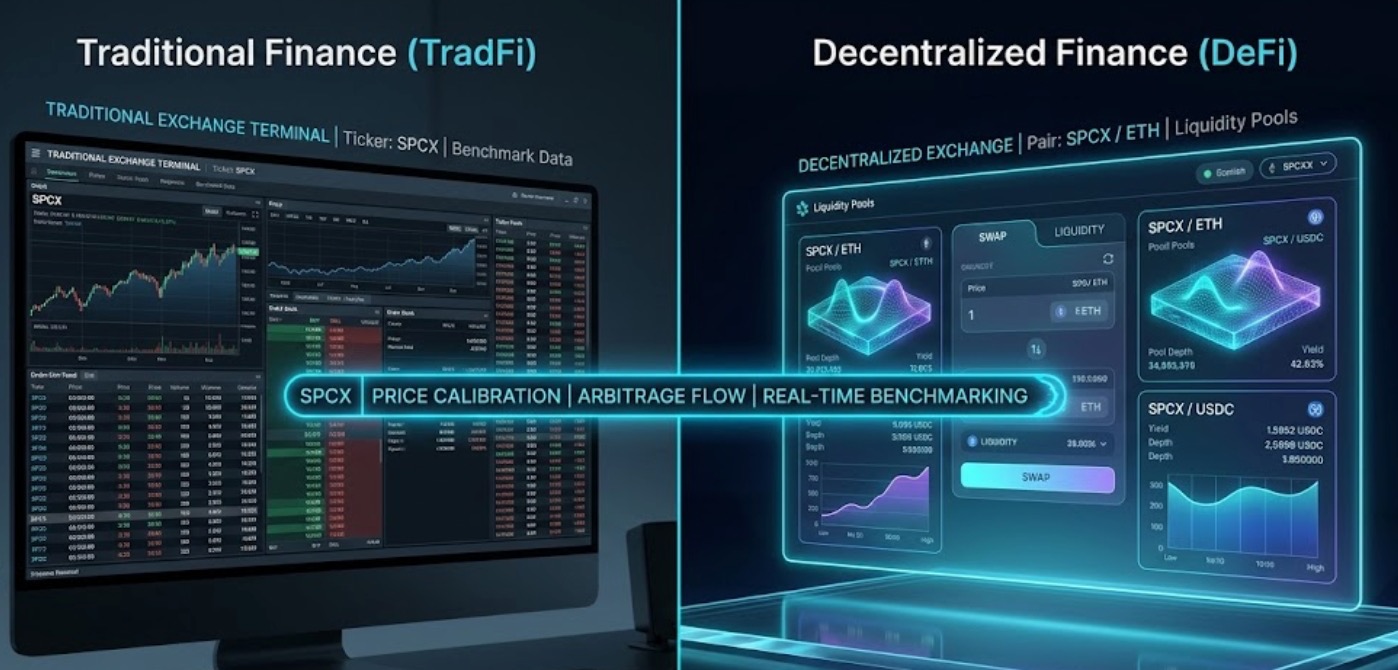

SPCX Gives Tokenized Stocks a Real Benchmark

The most important change after the IPO is simple: SpaceX now has a public quote.

That matters because tokenized SpaceX products can no longer rely only on the pre-IPO narrative. Users can compare them against public SPCX shares.

If a tokenized SpaceX product trades far above the public stock price, traders should ask why. Is it because of limited supply? Different trading hours? A funding effect? A platform-specific pricing model? Thin liquidity? Speculative demand?

If it trades below the public quote, the questions are just as important. Is there a redemption limit? Is the market illiquid? Is the issuer using a different reference price? Are holders unable to convert the token into the underlying stock?

A public stock price does not eliminate confusion. It exposes it. That is why SPCX may become one of the most important examples in the tokenized equity market. It gives traders a high-profile asset where the difference between price exposure and ownership can no longer be ignored.

Tokenized Stock Does Not Always Mean Stock Ownership

The phrase “tokenized stock” sounds straightforward. In reality, it can mean several different things. Some products may be backed by real shares held through a custodian. Some may offer redemption into shares or cash, depending on user eligibility and platform rules. Others may be synthetic products that track a reference price but do not give users any direct claim on the underlying equity.

That distinction is the whole story. Owning public SPCX shares through a broker is one type of exposure. Holding a tokenized SpaceX product is another. Trading a perpetual contract or derivative linked to SpaceX price movement is something else entirely.

They may all move around the same headline. They do not all give users the same rights.

Public shares may come with shareholder rights, depending on the broker and account structure. Tokenized stocks depend on the issuer, custody model, and redemption rules. Derivatives usually provide price exposure only.

A trader can profit from price movement without owning the company. But they should know that is what they are doing.

Why Crypto Traders Rushed Toward SpaceX Exposure

SpaceX has the kind of brand power that crypto markets understand immediately.

It has Elon Musk. It has Starlink. It has reusable rockets. It has Mars ambition. It has AI links. It has a massive retail following and a company story that feels bigger than a normal aerospace business.

That combination made it a natural fit for tokenized stock demand.

Crypto traders are used to 24/7 markets, stablecoin settlement, fast access, and narrative-driven positioning. SpaceX fits that environment better than most traditional stocks. It is not surprising that tokenized SpaceX products drew heavy attention as soon as the IPO approached.

But strong demand can also reveal weak infrastructure.

Some tokenized SpaceX campaigns reportedly had to refund users because there were not enough underlying shares available to support promised allocations. That is an important moment for the RWA market. It shows that on-chain demand can appear instantly, but the real-world asset still has to be sourced, held, settled, and reconciled through traditional systems.

Tokenization does not magically create unlimited stock supply.

SpaceX Is Becoming an RWA Pressure Test

The RWA market has spent years arguing that stocks, bonds, funds, commodities, and private-market exposure can move on-chain.

SpaceX is putting that idea under pressure in real time.

On one side, the demand is obvious. SpaceX tokenized products have attracted major attention, and some venues saw unusually large trading volume compared with other tokenized equities. That tells us crypto users want access to traditional market stories when the asset is exciting enough.

On the other side, the friction is also obvious. Issuers need access to shares. Platforms need reliable pricing. Users need to understand redemption. Regulators care about investor eligibility. Liquidity can vary sharply between products. A token can trade smoothly on-screen while the legal and operational structure underneath remains complicated.

That is the reality of tokenized equities.

The technology can make the wrapper faster. It does not remove the need for custody, compliance, transparency, and market structure.

The Premium and Discount Problem

One of the biggest things to watch is the gap between public SPCX and tokenized SpaceX products.

In theory, a fully backed and redeemable tokenized stock should stay close to the public share price, after accounting for fees, trading hours, and market conditions. In practice, differences can appear quickly.

A tokenized product may trade at a premium if users want 24/7 access and supply is limited. It may trade at a discount if users doubt the issuer, cannot redeem easily, or if liquidity is thin.

For traders, that gap is not just a number. It is information.

A large premium may signal strong demand, but it may also mean buyers are paying too much for convenience. A large discount may look like an opportunity, but it may reflect structural limits that are not easy to arbitrage.

This is why users should not assume that every SpaceX-linked product is interchangeable.

The ticker may look familiar. The risk may not be.

Bottom Line

SpaceX’s IPO turned SPCX into more than a public stock ticker.

It became a live test for tokenized equities. Crypto traders clearly want SpaceX exposure. Platforms clearly want to offer it. RWA issuers clearly see the opportunity. But the early activity also shows why users need to be careful.

Public SPCX shares, tokenized SpaceX stock, Ondo-style tokenized versions, platform derivatives, and perpetual futures may all follow the same SpaceX story. They do not all carry the same rights, pricing logic, liquidity, or risks.

That is the lesson.

Tokenized stocks may be part of the future of markets. SpaceX is helping prove the demand. Now the industry has to prove the structure.

For traders, the safest starting point is simple: compare every SpaceX-linked product against public SPCX, read the product terms, understand whether there is real backing or only price exposure, and never confuse a tradeable token with automatic shareholder ownership.

Explore the latest markets on Tapbit, log in to trade, or create an account to get started.

Frequently Asked Questions (FAQ)

What is SpaceX tokenized stock?

SpaceX tokenized stock is a digital product designed to give users exposure to SpaceX-related equity value. The exact structure depends on the issuer. Some products may be backed by real shares, while others may be synthetic products, derivatives, or price-tracking instruments.

Is SpaceX tokenized stock the same as SPCX stock?

Not always. SPCX is the public stock ticker for SpaceX shares traded on the stock market. A tokenized SpaceX product may track SPCX price movement, but that does not automatically mean the holder owns public SpaceX shares.

Why does the SpaceX IPO matter for tokenized stocks?

Before the IPO, many SpaceX-linked products were built around private-market or pre-IPO access. After the IPO, SPCX became a public benchmark. This makes it easier for users to compare tokenized SpaceX products against the real public stock price.