India’s July 8 stock market selloff showed how quickly geopolitical risk can move from the Strait of Hormuz into oil prices, exchange rates and equity valuations.

Indian stocks suffered one of their sharpest sessions in months on July 8, 2026.

The BSE Sensex dropped 1,677.12 points, or 2.15%, to close at 76,503.60. The NSE Nifty 50 fell 516.65 points, or 2.12%, finishing at 23,882.05. Official exchange data confirmed the scale of the decline, while volatility rose sharply as investors reduced exposure across banking, automobile, aviation and consumer-related shares.

The immediate trigger was a fresh escalation between the United States and Iran. Speaking at the NATO summit in Ankara, US President Donald Trump said that the interim agreement intended to pause the conflict with Iran was effectively “over.” His comments came after renewed military action and attacks involving commercial shipping near the Strait of Hormuz.

However, Trump’s statement alone does not fully explain why Indian equities reacted so strongly.

The deeper issue is India’s dependence on imported energy. When conflict threatens oil supplies in the Middle East, the effects can quickly spread into India’s currency, inflation outlook, interest-rate expectations and corporate earnings.

What Triggered the Indian Stock Market Selloff?

Markets rarely respond to a political statement in isolation. They react to what that statement could mean for future economic conditions.

Trump’s remarks increased concern that the US–Iran conflict could continue or intensify. Investors immediately began pricing in several risks:

-

Potential interruptions to oil shipments

-

Higher crude oil prices

-

Increased shipping and insurance costs

-

A stronger US dollar

-

Pressure on oil-importing economies

-

Reduced appetite for riskier assets

For Indian investors, oil was the most important part of that calculation.

India imports close to 90% of the crude oil it consumes. Estimates for the 2025–26 financial year placed its import dependence at around 88.6% or higher, depending on the measurement period used.

That leaves the country especially exposed when global oil prices rise unexpectedly.

Why Rising Oil Prices Matter So Much for India

An increase in crude oil prices can affect India through several channels at the same time.

First, the country must spend more foreign currency to pay for its energy imports. That increases demand for US dollars and can weaken the Indian rupee.

Second, higher fuel costs feed into transportation, manufacturing, aviation, agriculture and consumer goods. Even companies that do not purchase crude oil directly can face higher logistics and production expenses.

Third, a prolonged oil shock can complicate monetary policy. The Reserve Bank of India may find it harder to lower interest rates if energy costs are pushing inflation higher.

Finally, investors may reduce their exposure to Indian assets if they expect weaker corporate margins, higher inflation or continued currency depreciation.

This creates a familiar transmission chain:

Geopolitical escalation → oil supply concerns → higher crude prices → rupee pressure → inflation risk → tighter financial conditions → weaker equity sentiment

The Reserve Bank of India has already identified global supply concerns, oil prices and geopolitical instability as important risks to India’s growth and inflation outlook. In June 2026, the central bank kept its repo rate unchanged at 5.25%, reflecting the difficult balance between supporting growth and containing inflation risks.

The Rupee Added Another Layer of Pressure

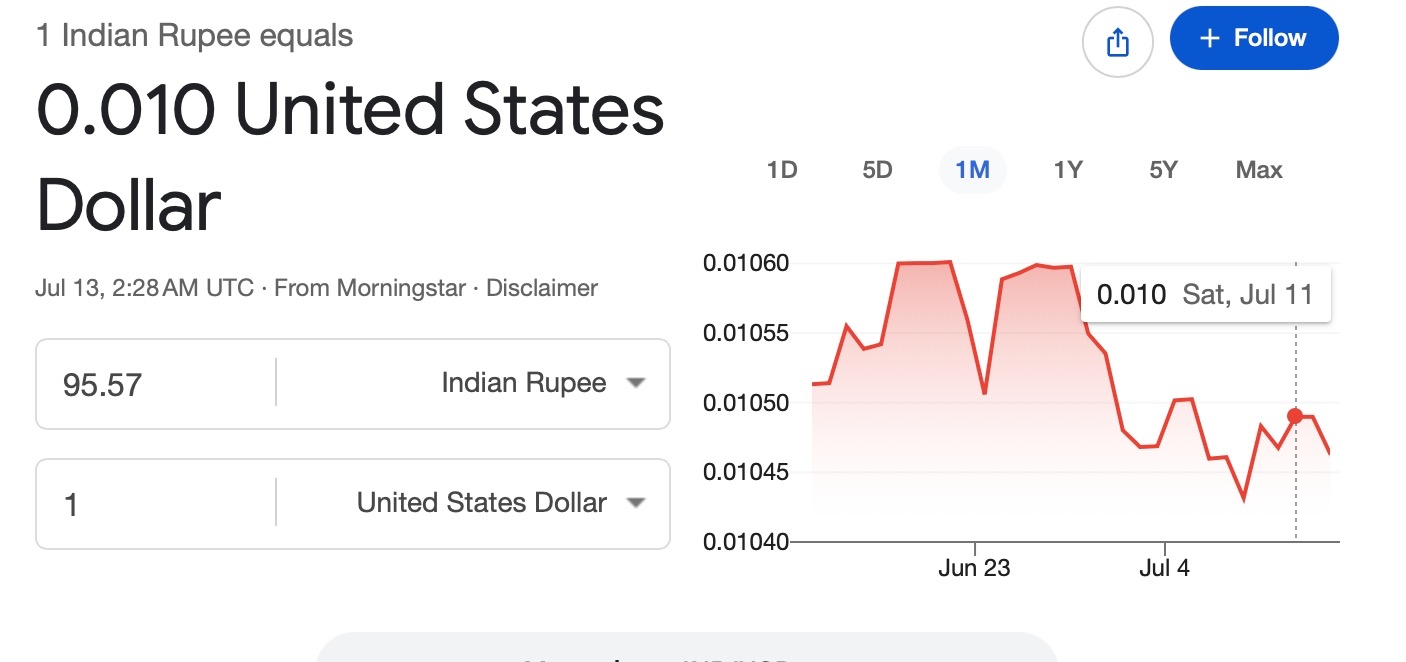

The Indian rupee also came under heavy selling pressure during the July 8 session.

It weakened by around 59 paise and closed near 95.55 against the US dollar, according to provisional market figures reported that day. The fall was linked to higher oil prices, dollar strength and concerns about further escalation in the Middle East.

A weaker rupee matters because oil is generally priced in US dollars.

When the rupee falls, Indian refiners and importers must pay more in local-currency terms, even when the dollar price of oil remains unchanged. If oil prices and the dollar rise simultaneously, the cost pressure becomes more severe.

Currency depreciation can also affect overseas investors. A foreign investor may earn a positive return on an Indian stock in rupee terms but still record a loss after converting the proceeds back into dollars.

That makes sustained rupee weakness a potential reason for foreign investors to reduce exposure.

Why the Strait of Hormuz Is Central to the Story

The Strait of Hormuz is not simply another regional shipping route. It is one of the most important energy chokepoints in the world.

According to the US Energy Information Administration, oil flows through the strait during 2024 and the first quarter of 2025 represented more than one-quarter of global seaborne oil trade and roughly one-fifth of worldwide petroleum consumption. Around one-fifth of global liquefied natural gas trade also passed through the route in 2024.

This means that even a temporary disruption can influence oil prices well beyond the Middle East.

Markets do not necessarily wait for shipments to stop completely. The possibility of disruption can be enough to increase freight rates, insurance premiums and speculative demand for crude oil.

For India, the risk is particularly relevant because a meaningful share of its crude oil and gas imports is connected to Gulf suppliers and shipping routes.

Which Indian Sectors Are Most Exposed?

The selloff was broad, but some industries are naturally more vulnerable to an oil shock.

Aviation

Fuel is one of the largest operating expenses for airlines. Higher crude and jet-fuel prices can rapidly weaken profit margins, especially if airlines cannot pass the full increase on to passengers.

Automobiles

Higher fuel prices can reduce demand for conventional vehicles, while a weaker rupee can increase the cost of imported parts and raw materials.

Logistics and Transportation

Trucking, shipping and delivery companies face higher fuel expenses. These costs may eventually be passed on to customers, adding to inflation.

Consumer Goods

Consumer businesses can be affected through packaging, transportation and production costs. At the same time, higher household fuel bills may reduce discretionary spending.

Banking and Financial Services

Banks are not directly exposed to oil prices in the same way as airlines, but they can suffer when higher inflation delays rate cuts, weakens loan demand or creates repayment pressure for energy-sensitive businesses.

Oil Producers and Refiners

The impact is more complicated for energy companies. Upstream producers may benefit from higher crude prices, while refiners can face volatile margins, higher working-capital requirements and policy-related uncertainty.

Was This a Fundamental Collapse in Indian Equities?

Not necessarily. The July 8 fall looked more like a broad risk-off event than a sudden breakdown in India’s long-term economic story.

Stocks declined across multiple sectors as investors reacted to a common external shock. This is different from a selloff driven by weak earnings at one company or a structural crisis in a specific industry.

The market also showed some ability to recover.

On July 9, the Sensex gained around 230 points as immediate fears eased. On July 10, the rebound became stronger, with the Sensex rising 828 points and the Nifty closing above 24,200. Better global sentiment, foreign investor buying and the start of India’s quarterly earnings season helped support the recovery.

The rebound does not mean the risk has disappeared. It shows that traders are reassessing the situation day by day rather than treating the conflict as a permanent change to India’s growth outlook.

What This Means for Crypto and Global Markets

The same macroeconomic forces affecting Indian equities can also influence cryptocurrencies.

Geopolitical uncertainty often causes investors to reduce leverage and move away from risk assets. Bitcoin and major altcoins may initially decline alongside equities when traders seek cash or reduce speculative positions.

However, crypto markets can also react differently depending on the nature of the crisis.

A weaker currency, capital-control concerns or declining trust in traditional financial systems can sometimes increase interest in Bitcoin, stablecoins and other digital assets. The outcome depends on liquidity conditions, monetary policy expectations and the duration of the conflict.

For this reason, traders should avoid assuming that Bitcoin will always behave as either a safe haven or a risk asset. Its market role can change over different time horizons.

Readers following global market volatility, crypto assets and major trading pairs can visit the official Tapbit platform. Existing users can access their accounts through the Tapbit login page, while new users can create an account through the Tapbit registration page.

Final Thoughts

Trump’s Iran remarks were the immediate headline behind the July 8 Indian stock market crash, but they were not the only reason Sensex and Nifty fell.

The market was reacting to a broader chain of risks involving the Strait of Hormuz, crude oil prices, India’s energy-import dependence, rupee weakness, inflation and monetary policy.

That distinction matters.

Political comments can trigger a rapid market move, but the duration of the selloff will depend on whether those comments lead to real supply disruptions, prolonged military escalation or lasting economic damage.

India’s long-term domestic growth drivers have not disappeared. At the same time, its dependence on imported crude means Middle East energy shocks will continue to be an important source of short-term volatility.

For now, crude oil, the rupee and shipping activity through the Strait of Hormuz may provide more useful signals than any single political headline.

Frequently Asked Questions

Why did Sensex and Nifty crash on July 8, 2026?

The indices fell after renewed US–Iran tensions increased concerns about oil supplies and global economic risk. Rising crude prices, a weaker rupee and broad investor risk reduction contributed to the decline.

How much did Sensex and Nifty fall?

Sensex dropped 1,677.12 points, or 2.15%, to 76,503.60. Nifty 50 lost 516.65 points, or 2.12%, and closed at 23,882.05.

Why do higher oil prices hurt the Indian stock market?

India imports most of the crude oil it consumes. Higher oil prices increase the import bill, pressure the rupee, raise inflation risks and increase operating costs for many companies.