Broadcom has become one of the most closely watched names in the AI semiconductor trade. After a strong run earlier this year, AVGO stock pulled back sharply from its recent highs, raising a familiar question for traders: is this a warning sign, or a buy-the-dip opportunity?

The answer is not simple. Broadcom’s latest earnings showed strong revenue growth, record AI semiconductor sales, and continued demand for custom AI chips. At the same time, the market had already priced in very high expectations. When guidance failed to surprise investors enough, AVGO sold off despite the company’s strong fundamentals.

For users following fast-moving technology and digital asset markets, Tapbit provides market access, trading tools, and educational resources to help users better understand major macro and sector-driven trends.

AVGO Stock Price: Why the Pullback Matters

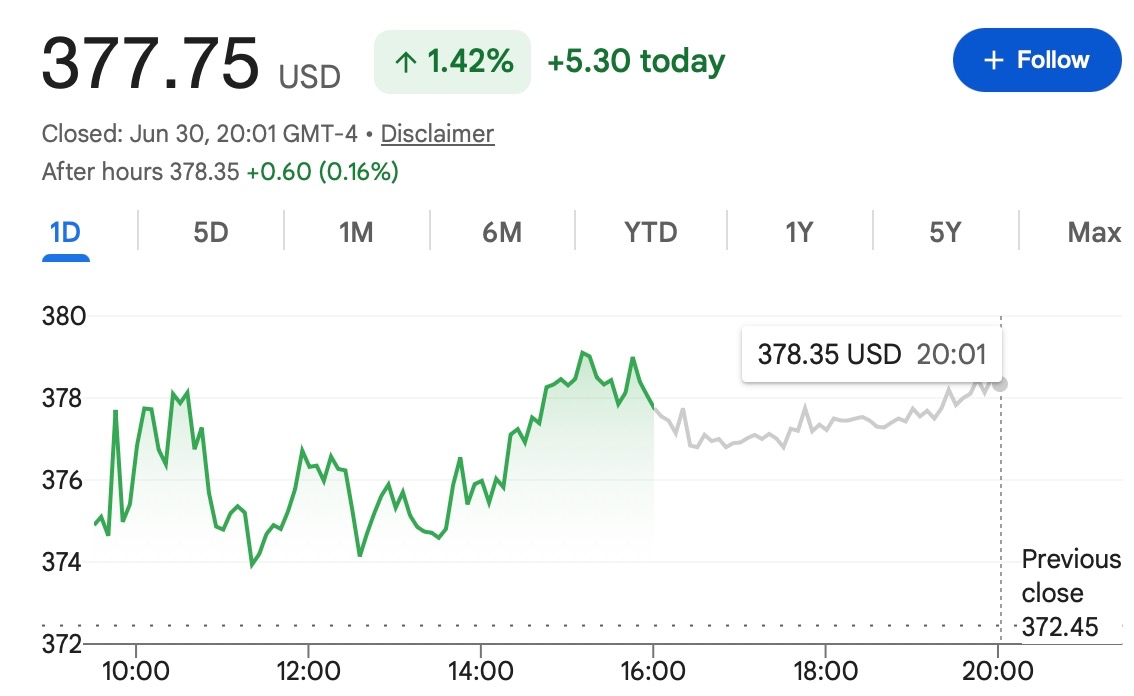

As of the latest available market data on July 1, 2026, Broadcom stock traded around $377.75, with a market capitalization of about $1.76 trillion. The stock was still up over the past year, but it had fallen more than 20% from its early June highs.

That pullback matters because Broadcom is not a weak business story. It is one of the most important companies in the AI chip supply chain, especially in custom AI accelerators, networking, advanced packaging, and infrastructure software. The stock decline shows how selective investors have become in the AI trade.

In 2024 and 2025, many AI-related stocks rose simply because they were connected to the AI infrastructure boom. In 2026, the market is asking harder questions: Can growth continue? Can margins hold up? Can large customers keep spending? And can companies still beat already aggressive expectations?

Broadcom’s Latest Earnings: Strong Numbers, Tough Expectations

Broadcom’s fiscal second-quarter 2026 results were strong on the surface.

The company reported revenue of $22.19 billion, up 48% year over year. Broadcom said the quarter was driven by accelerating AI semiconductor revenue and strong operating leverage.

The AI numbers were even stronger. Broadcom reported AI semiconductor revenue of $10.8 billion, up 143% from the previous year. For the fiscal third quarter, the company expects AI semiconductor revenue to reach $16 billion, representing more than 200% year-over-year growth.

Normally, those numbers would look impressive. But AVGO stock still fell after earnings because investor expectations were already extremely high. Some traders wanted even stronger long-term guidance, especially after the stock had rallied sharply earlier in the year.

That is the key lesson from Broadcom’s pullback: in the AI chip market, strong growth may no longer be enough. Investors increasingly want growth that beats already elevated expectations.

Why Analysts Still Like Broadcom

Despite the sell-off, several Wall Street analysts remain positive on AVGO.

Investopedia reported that Jefferies maintained a Buy rating with a $550 price target, while JPMorgan kept an Overweight rating with a $580 price target. Both firms viewed the pullback as a potential buying opportunity rather than a sign that Broadcom’s AI story is broken.

JPMorgan’s bullish view is based on Broadcom’s strength in custom AI chips, advanced chip design, packaging, and networking. These areas are becoming more important as large technology companies look for alternatives or complements to traditional GPU-based AI infrastructure.

This does not mean AVGO is risk-free. It means analysts are distinguishing between short-term stock pressure and long-term demand for AI infrastructure.

OpenAI Custom Chip News Adds to the AI ASIC Story

One of the most important recent developments is Broadcom’s reported work with OpenAI on a custom AI chip.

MarketWatch reported that Broadcom and OpenAI introduced a custom chip called “Jalapeño,” designed for AI inference workloads. The report said the chip is part of OpenAI’s broader effort to build more efficient AI infrastructure and reduce dependence on existing GPU supply chains.

This matters because AI inference is becoming one of the most important parts of the AI economy. Training large models is expensive, but inference is the ongoing cost of serving users every day. If companies like OpenAI can improve inference efficiency through custom chips, Broadcom could benefit as a key ASIC partner.

For Broadcom, this strengthens the long-term thesis that AI infrastructure will not be only about GPUs. Custom silicon, networking, memory systems, and advanced packaging may all become critical parts of the next AI cycle.

AVGO 2026 Outlook: What Could Push the Stock Higher?

The bullish case for AVGO depends on three main points.

First, Broadcom’s AI semiconductor revenue needs to keep scaling. The company’s Q3 guidance for $16 billion in AI semiconductor revenue shows that demand remains strong, but investors will want confirmation in future quarters.

Second, custom AI chip customers need to expand. Broadcom already has a strong position in custom silicon, and new customer relationships could support long-term growth if AI workloads continue shifting toward application-specific chips.

Third, VMware and infrastructure software need to keep supporting cash flow. Broadcom is not only an AI chip company. Its software business gives it a broader earnings base, which may help reduce reliance on semiconductor cycles over time.

If these factors hold, AVGO could remain one of the leading AI infrastructure stocks in 2026.

Main Risks to Watch

The first risk is valuation. AVGO remains a large-cap AI leader, and the market is already pricing in years of strong growth. If future guidance disappoints, even slightly, the stock may remain volatile.

The second risk is customer concentration. Broadcom’s custom AI chip business depends heavily on large technology customers. If any major customer delays orders, changes suppliers, or reduces spending, the market reaction could be sharp.

The third risk is competition. Nvidia remains dominant in AI accelerators, while AMD, Marvell, Google, Amazon, Microsoft, and other players are also investing heavily in custom AI hardware. Broadcom’s opportunity is large, but the field is competitive.

The fourth risk is margin pressure. Custom AI systems and advanced packaging can support strong revenue growth, but investors will watch whether product mix changes affect profitability.

The fifth risk is expectation risk. Broadcom’s recent decline shows that a company can deliver strong numbers and still see its stock fall if the market was expecting even more.

What AVGO Means for Market Traders

AVGO is now a good example of how the AI trade is changing.

The first phase of the AI rally was about identifying companies with exposure to AI demand. The next phase is about separating companies that can turn AI demand into durable revenue, high margins, and repeatable customer relationships.

Broadcom remains well positioned in custom AI chips, networking, and infrastructure software. But its stock price will likely depend on whether future earnings reports can prove that current AI demand is not just a short-term spending wave.

For Tapbit users watching broader market themes, AVGO is worth following because it reflects investor sentiment toward AI infrastructure. When AVGO rises, it can signal renewed confidence in AI chip demand. When it falls, it may show that markets are becoming more cautious about valuations and expectations.

Existing users can log in to Tapbit to follow market opportunities, while new users can register on Tapbit to explore available trading features and educational resources.

Final Thoughts

Broadcom’s stock pullback does not necessarily mean the AI chip story is over. The company continues to report strong AI semiconductor growth, and analyst sentiment remains broadly positive. The recent sell-off is more about expectations than a collapse in fundamentals.

Still, traders should not ignore the risks. AVGO is a high-expectation stock in a high-competition sector. Future performance will depend on AI revenue growth, customer expansion, execution, margins, and whether the market continues to reward AI infrastructure leaders.

The clearest takeaway is this: AVGO remains one of the most important AI chip stocks to watch in 2026, but the market is no longer rewarding AI exposure alone. From here, Broadcom needs to keep proving that custom AI chips can become a durable growth engine.

Frequently Asked Questions (FAQ)

What is AVGO?

AVGO is the stock ticker for Broadcom Inc., a major semiconductor and infrastructure software company. Broadcom is widely followed for its role in AI chips, custom silicon, networking solutions, and enterprise software.

Why did AVGO stock price pull back?

AVGO stock price pulled back because market expectations for AI chip growth had become very high. Broadcom reported strong earnings and rapid AI semiconductor revenue growth, but some investors expected even stronger guidance. The decline was more about high expectations than a clear collapse in fundamentals.

Is Broadcom still benefiting from AI demand?

Yes. Broadcom continues to benefit from demand for custom AI chips, AI networking, advanced packaging, and data center infrastructure. Its AI semiconductor revenue has grown sharply, showing that the company remains an important part of the AI infrastructure supply chain.