If you've been trading crypto long enough, you have probably heard the "XRP will replace SWIFT" narrative so many times it just sounds like white noise. For years, it was easy to dismiss this as pure retail speculation or bag-holder coping.

But here on Tapbit, we don't trade sentiment or Reddit rumors; we trade structural shifts in market plumbing.

Over the last few weeks, documented evidence has surfaced confirming that Ripple’s strategy to embed itself into the global banking system is actively materializing. This isn't an "AI hallucination" or a speculative whitepaper—it is backed by live pilot data and institutional on-chain mechanics.

Here is the hard, verifiable data on why XRP’s threat to SWIFT is finally maturing, and how you should position your portfolio.

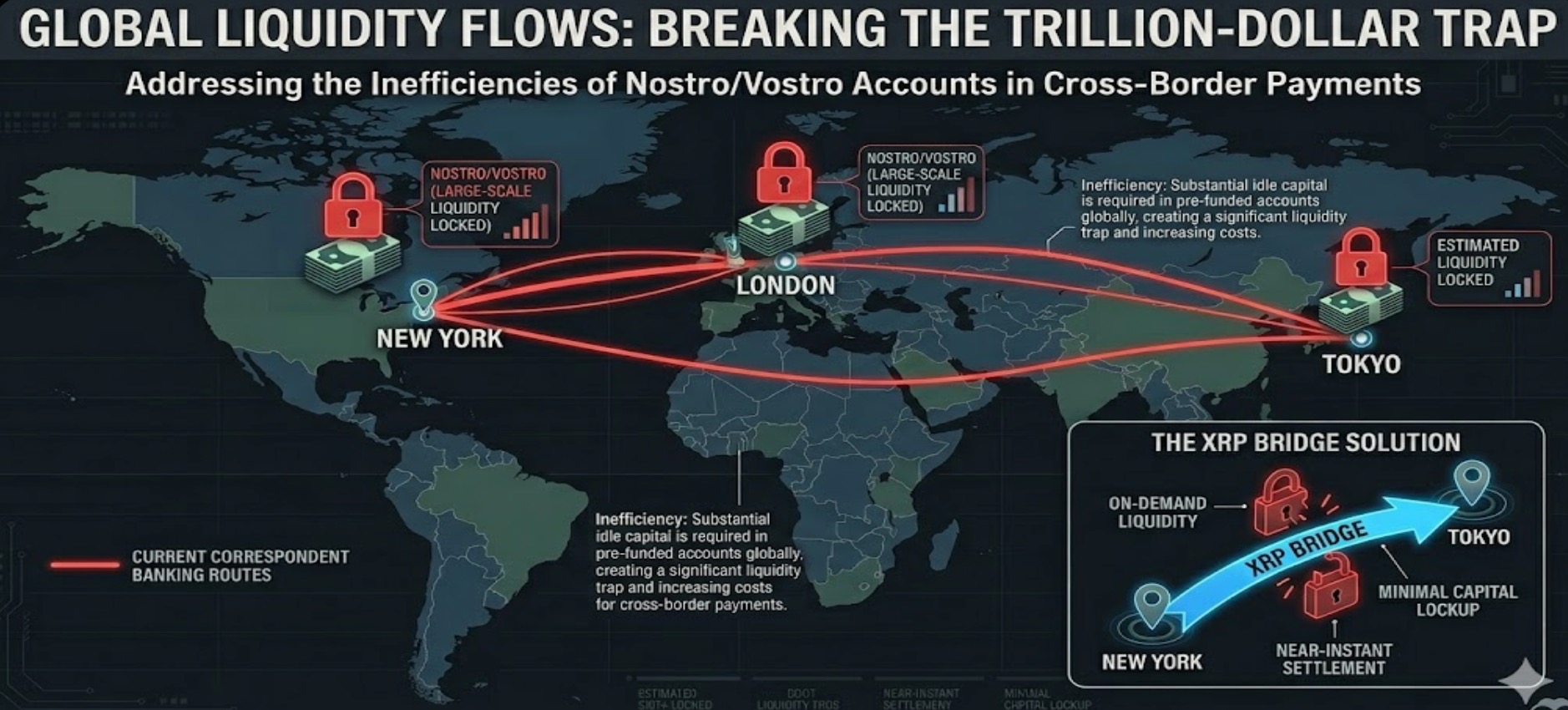

The Core Trap: Nostro/Vostro Accounts

To understand why traditional finance needs XRP, you have to understand why the current system is broken.

SWIFT is the backbone of global finance, moving $5 trillion daily. But as recently highlighted by crypto researchers reviewing strategic documents, SWIFT is not a settlement system; it is a 1970s messaging protocol. When a bank sends money internationally, the actual capital doesn't "move." Instead, banks rely on pre-funded "nostro and vostro" accounts. They literally have to park trillions of dollars in foreign banks across different time zones just to have the liquidity ready to clear those SWIFT messages.

Ripple’s documented vision uses XRP as a "bridge asset" to eliminate this trap. A bank converts fiat to XRP, moves it across the RippleNet ledger in 3-5 seconds, and converts it back to the local fiat on the receiving end. No dormant capital. No expensive correspondent banking fees.

The Evidence: Leave the Rumors, Look at the Links

The critique of XRP has always been that banks would never use a volatile crypto asset. Recent market developments have invalidated that argument. Here is the authoritative data showing XRP's infiltration into traditional finance:

-

The Japanese Bank Pilots (Live Data): This isn't theoretical. According to real-time market reporting from The Crypto Basic and DailyCoin, Japanese banks recently released live data comparing the two systems. The results? Using XRP slashed settlement costs by 60% compared to SWIFT, with absolute finality in under 4 seconds (compared to SWIFT's 1-to-5 business days).

-

ISO 20022 Integration: The global banking system is currently undergoing a mandatory upgrade to the SWIFT ISO 20022 messaging standard. Official documentation confirms that XRP is one of the few digital assets actively aligned and natively compliant with this exact standard. It is built to plug directly into the banks' new software systems.

-

Institutional Acknowledgement: Wall Street is quietly admitting the transition. Matthew Le Merle, an Advisory Board Director at Bitwise, recently noted in an industry presentation that legacy systems like SWIFT and Visa are actively being "upgraded into digital equivalents, which have names like Ripple."

The Trader's Edge: How to Play the Transition

This is the kind of fundamental shift that triggers massive repricing, but it does not happen overnight.

Right now, the broader market is severely underpricing XRP's institutional traction because retail traders are too busy chasing pump-and-dump meme coins. Smart money, however, is quietly accumulating spot XRP during these low-volatility, sideways consolidation phases.

How to execute this on Tapbit:

-

Avoid the High-Leverage Chop: XRP is notorious for frustrating, drawn-out ranges followed by sudden, violent green candles. If you try to aggressively long XRP with 50x leverage right now, market makers will likely hunt your stop-losses before the real macro breakout happens.

-

Spot Accumulation & Grid Bots: The smartest institutional play here is patience. Build a spot position near major historical support levels, or run a Grid Trading Bot on Tapbit. A grid bot will automatically buy the micro-dips and sell the micro-pumps within the current range, allowing you to farm yield while waiting for the macro breakout.

Stop fighting the noise and the rumors. Trade the infrastructure.

Log in to the Tapbit terminal today to set up your grid bots and position yourself ahead of the global liquidity shift.

Frequently Asked Questions (FAQ)

What is the main problem with the current SWIFT system?

SWIFT is fundamentally a 1970s messaging protocol, not a settlement network. To move money internationally, banks are forced to pre-fund "nostro and vostro" accounts in foreign jurisdictions. This archaic structure locks up trillions of dollars in dormant capital and takes days to clear. XRP solves this by acting as a direct bridge asset, settling the actual capital in seconds and eliminating the need for these expensive pre-funded accounts.

Aren't banks afraid of XRP's price volatility?

This is a common retail misconception. Banks do not hold XRP as a speculative investment in this process; they use it purely as a transitional bridge. Because the RippleNet ledger achieves absolute finality in just 3 to 5 seconds, the exposure window for price volatility to impact the transfer value is practically zero.

Is there verifiable proof that XRP is actually cheaper or faster than SWIFT?

Yes. Recent live pilot data released by Japanese financial institutions directly compared the two systems in real-world remittance corridors. The empirical results showed that using XRP slashed overall settlement costs by 60% and completed transactions in under 4 seconds, vastly outperforming SWIFT's standard 1-to-5 business day timeline.